March Market Insights

Market Transitions

Over the past three weeks, U.S Large Cap stocks have steadily decreased pushing the Nasdaq across the correction threshold while the S&P 500 is in the neighborhood. A correction is defined as a 10% drawdown from the recent high. While this is noteworthy and is dominating headlines, it is not actually out of the ordinary. Over the past 40 years, the median intra-year drawdown for the S&P 500 is 10%.1 Corrections, while uncomfortable, are an inherent part of the normal functioning of the markets. The factors driving this market pressure are varied. Market concentration, institutional trade unwinding, and trade policy are all playing a part in influencing investor sentiment.

Market Concentration and Repositioning

A key theme in the market since 2023 has been the premium at which Mega Cap stocks traded and their relative dominance of the index. As of February 28th, 2025, the top-10 companies in the S&P 500 accounted for 36.4% of the index market capitalization.2

Source: J.P. Morgan Asset Management3

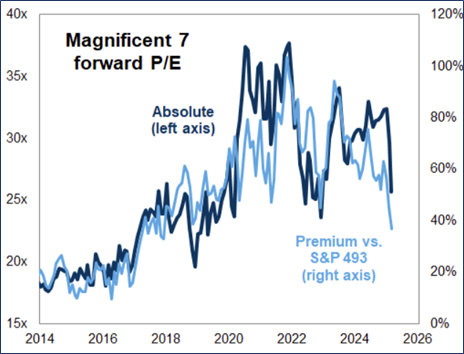

Furthermore, until recently, the Magnificent 7 traded at a roughly 80% premium in their forward Price to Earnings ratios when compared against the rest of the index. As of the market close on Tuesday, March 11, that premium has reduced to roughly 50%, its lowest level since 2017.4

Source: Goldman Sachs.5

On Friday, March 7, hedge funds began de-levering themselves at a quicker pace, adjusting positioning to align with other risks, namely trade policy and growth, in the market.6 This unwinding played a significant role in the market decline since Friday. The quick reshaping of valuations has rapidly changed the premium conversation. Some estimates suggest that the S&P 500 is now trading at its fair-value Price to Earnings multiple.7

Tariffs

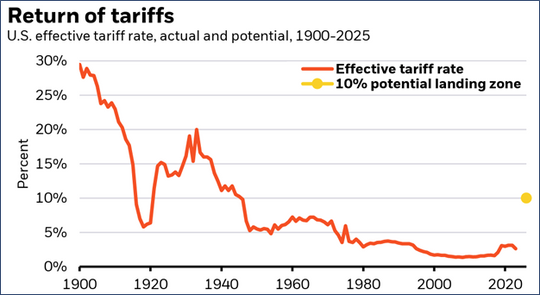

While tariff events over the past few months have caused volatility, activity in the last week appears to be, in part, from the realization that the administration is likely to be more intransigent on tariffs than the market expected.8 Current estimates are that the effective tariff rate may settle around 10%.9

Source: BlackRock.10

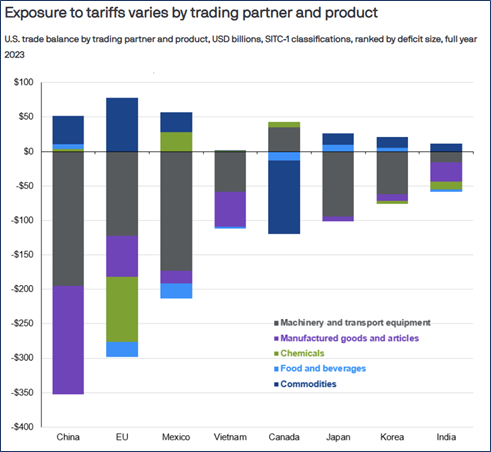

This figure, of course, is variable, and depends on what tariffs are implemented as negotiation objectives are met or missed. It is critical to remember that tariffs have historically increased inflation in the short term, but left much less of an impact in the long term.11 The chief risk, however, is that if tariffs remain in place for an extended period of time, they could in turn reduce demand and thereby suppress growth. Like inflation, the impact of tariffs on growth is generally short-lived, but the longer tariffs remain in place the greater an effect they may have.12

Source: J.P. Morgan Asset Management.13

Important Data

February non-farm payroll employment rose by 151,000 jobs and the unemployment rate held at 4.1%.14 This report came in slightly below expectations but beat January’s numbers by 25,000 jobs.15 Wednesday’s Consumer Price Index release indicated that inflation rose at 2.8% for the year ending in February.16 That is 0.2% lower than the yearly reading through January and 0.1% lower than consensus expectations.17 This reading buoyed the stock market on Wednesday. The Bureau of Economic Activity will release its February Personal Consumption Expenditures Price Index reading, the Fed’s preferred inflation gauge, on March 28th.

The Bright Spots

There are bright spots in the market despite the headlines. Foreign developed markets, especially in Europe, have performed very well. Specifically, with increased defense spending proposals from European countries, European defense and aerospace companies have rallied.18 European banks have continued a strong run, benefitting from higher interest rates and fee income.19 Notably, U.S. Large Cap Value stocks have served as a bellwether in the face of uncertainty. Core Bonds have also performed well, outpacing U.S. equity year to date.20 These are all areas of relative outperformance that demonstrate the benefit of a diversified portfolio in times of volatility.

We do expect volatility to continue in the short-term. Despite this, and while there has been some softening, economic growth remains the expectation. Though news headlines since the weekend have stoked fears of recession, current drawdowns are nowhere near the expected losses that come with a recession.21 Current estimates place the likelihood of recession in the next 12 months between 20% and 25%, only slightly elevated above the historical average of 15%.22

Citations:

1) Kostin, D et al. U.S Equity Views. Goldman Sachs, March 11, 2025.

2) Kelly, D. et al. Guide to the Markets. J.P. Morgan Asset Management, February 28, 2025.

3) IBID.

4) Kostin, D et al. U.S Equity Views. Goldman Sachs, March 11, 2025.

5) IBID.

6) Mandl, C. Hedge funds sped up de-risking, and there likely is more to come. Reuters, March 12, 2025.

7) Kostin, D et al. U.S Equity Views. Goldman Sachs, March 11, 2025.

8) Janasiewicz, J and Melson, G. The Near-Term Roadmap. Natixis, March 12, 2025.

9) Boivin, J. et al. Weekly Commentary. BlackRock, March 10, 2025.

10) IBID.

11) Hooper, K. Tariffs rattle stock markets, but what’s the long-term impact? Invesco, February 4, 2024.

12) IBID.

13) Santos, G. What are the investment implications of higher tariffs? J.P. Morgan Asset Management, March 4, 2025.

14) U.S. Bureau of Labor Statistics. Employment Situation Summary. U.S. Department of Labor, March 7, 2025.

15) Lahart, J. U.S. Added 151,000 Jobs Last Month. The Wall Street Journal, March 7, 2025.

16) U.S. Bureau of Labor Statistics. Consumer Price Index Summary. U.S. Department of Labor. March 12, 2025.

17) Lahart, J. Inflation Cooled to 2.8% in February, Lower than Expected. The Wall Street Journal, March 12, 2025.

18) Edwards, N. and Durham, M. What’s driving Eurozone equity returns this year? J.P. Morgan Asset Management, March 12, 2025.

19) IBID.

20) BlackRock. Student of the Market. BlackRock, March, 2025.

21) Kostin, D et al. U.S Equity Views. Goldman Sachs, March 11, 2025.

22) IBID.

Important Information

The Clifford Group LLC (“The Clifford Group”) is a registered investment advisor. Advisory services are only offered to clients or prospective clients where The Clifford Group and its representatives are properly licensed or exempt from licensure. All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability, or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. The views expressed in this commentary are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur. The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your attorney or tax advisor. The information contained above is for illustrative purposes only.

For additional information, please visit our website at www.thecliffordgrp.com.

Risk Disclosure

No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. All investments include a risk of loss that clients should be prepared to bear. The principal risks of The Clifford Group strategies are disclosed in the publicly available Form ADV Part 2A. Diversification does not ensure a profit or guarantee against loss. Risk associated with equity investing include stock values which may fluctuate in response to the activities of individual companies and general market and economic conditions. Although bonds generally present less short-term risk and volatility risk than stocks, bonds contain interest rate risks; the risk of issuer default; issuer credit risk; liquidity risk; and inflation risk. Investing in foreign domiciled securities may involve risk of capital loss from unfavorable fluctuation in currency values, withholding taxes, from differences in generally accepted accounting principles or from economic or political instability in other nations. Investments in emerging or developing markets may be more volatile and less liquid than investing in developed markets and may involve exposure to economic structures that are generally less diverse and mature and to political systems which have less stability than those of more developed countries.