April Market Insights

Where We Stand

While the day-to-day landscape of tariffs and the broader economy has shifted rapidly over the last two weeks, and we have seen significant intraday price swings in both directions, markets remain in a similar position to where they were immediately following the “liberation day” tariff announcement. It appears that China is, and will remain, the primary sticking point in tariff negotiations. Though the administration seems willing to negotiate quickly with many of the trade partners named in the original April 2 announcement, it is likely that negotiations with China will come down to firm requirements and may have implications beyond trade policy alone.

On April 9, the White House paused country-specific tariffs for nearly all nations except China.¹ This sparked sharp market reactions, first driving prices higher on Wednesday, followed by selling pressure on Thursday as the market absorbed the reality of increased tariffs on Chinese goods. The pause likely brings the effective tariff rate down to approximately 15 percent.² Following the announcement, Wall Street analysts revised their forecasts away from worst-case recession scenarios, returning to more moderate, non-recessionary expectations.³ Current GDP growth estimates now project a gain of roughly 0.5 percent for the year.⁴

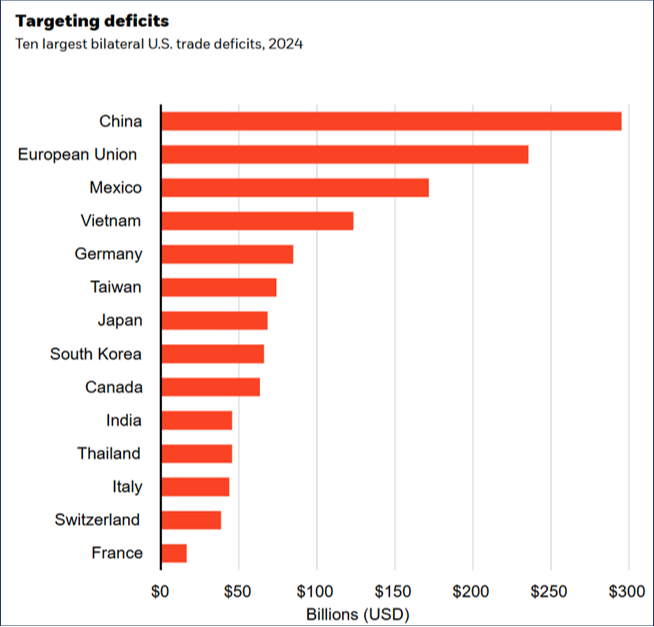

Source: BlackRock Investment Institute and U.S. Census Bureau, with data from Haver Analytics, April 2025. Note: The chart shows the ten largest trade deficits – the difference between U.S. goods imports and exports with a country – in 2024. The trade deficit for the European Union (EU) is the sum of the trade deficits across all EU members.5

U.S. Treasury yields have also experienced extreme volatility. On April 4, the 10-year yield hit a low of 3.87 percent—its lowest point since last October. Just one week later, it climbed to a recent high of 4.59 percent, before settling back to 4.33 percent, roughly the same level as prior to the April 2 tariff announcement. Several dynamics are driving this volatility. First, Federal Reserve Chair Powell has remained consistent in emphasizing that inflation will guide the pace of rate cuts, raising the possibility of fewer cuts than previously expected.⁶ At the same time, hedge funds engaged in an arbitrage trade shorting treasury futures and buying cash bonds with leverage were forced to start liquidating their positions as yields rose to fund margin calls and funding obligations, which only caused them to rise further.7 Additionally, investor sentiment, particularly among foreign investors, appears to be shifting, with a growing demand for higher yields to compensate for the rising national debt and an uncertain short-term outlook.⁸ During this period of volatility, gold has served as a primary safe haven.⁹

Key Information to Watch

March economic data remained strong, and April’s data releases will be critical for gauging how policy changes are affecting the broader economy. The NFIB Small Business Optimism Index declined in March but remains only slightly below the long-term average.10 Notably, two encouraging signs from the NFIB survey were that small business plans for capital investment and current job openings each increased by 2 percent.11 While the University of Michigan’s Consumer Sentiment Index reflected a decline in consumer expectations, big bank earnings reports indicated increased consumer spending in the first quarter.12 Though many respondents voiced pessimism about the direction of the economy, their spending behavior did not mirror that sentiment. In March, the U.S. economy added 228,000 jobs, and the unemployment rate ticked up slightly to 4.2 percent.13 A bright spot in the employment picture is the continued stability in the layoff rate.14 Although hiring has slowed somewhat, the hiring rate still exceeds the layoff rate, which has remained relatively unchanged. Looking forward, inflation metrics, labor market reports, and corporate earnings guidance will all play important roles in assessing the broader economic impact of the evolving tariff landscape.

Source: US Bureau of Labor Statistics, Haver Analytics, Goldman Sachs Global Investment Research.15

Equities

U.S. large growth stocks, and most notably the Magnificent 7, have faced particular pressure in the aftermath of tariff announcements. Three quarters of the Magnificent 7’s suppliers are located overseas, largely in East and Southeast Asia, and some component companies generate over half of their revenue abroad.16 Despite these facts, they remain supported by two of the largest thematic mega forces in the market right now: AI and cloud computing. The forward price-to-earnings ratio of the Magnificent 7 declined from 31 to 22 in early April, marking its lowest level since before the AI trade took off in 2023.17 Although trade policy may create short- to medium-term headwinds for earnings, analysts still project 15 percent earnings growth for the group in 2025.18 This underscores that while companies may face near-term challenges from shifting trade policies, long-term thematic trends remain intact.

Citations

1) President Donald Trump. Modifying Reciprocal Tariff Rates To Reflect Trading Partner Retaliation and Alignment. The White House, April 9th, 2025.

2) Hatzius, J. Global Views: Less Exceptional. Goldman Sachs, April 14th, 2025.

3) Hatzius, J, et al. USA: President Trump Announces 90 Day Pause; Reverting to Our Previous Non-Recession Baseline. Goldman Sachs, April 9th, 2025.

4) Hatzius, J. Global Views: Less Exceptional. Goldman Sachs, April 14th, 2025.

5) Boivin, J, et al. Weekly Commentary. BlackRock, April 14th, 2025.

6) Jackson, Jordan. Why are U.S Treasury Yields Rising? J.P. Morgan Asset Management, April 16th, 2025.

7) IBID.

8) Goldman Sachs. Why U.S. Treasuries Sold Off When Market Volatility Jumped. Goldman Sachs, April 17th, 2025.

9) Boivin, J, et al. Weekly Commentary. BlackRock, April 14th, 2025.

10) NFIB. Small Business Optimism Index. NFIB, April 8th, 2025.

11) IBID.

12) Glickman, B. and Saeedy, A. Big Banks Show Consumers Remained Resilient Heading Into Tariff Turmoil. The Wall Street Journal, April 15th, 2025.

13) Bureau of Labor Statistics. The Employment Situation- March 2025. The U.S. Department of Labor, April 4th, 2025.

14) Hatzius, J. Global Views: Less Exceptional. Goldman Sachs, April 14th, 2025.

15) IBID.

16) Aliaga, Stephanie. How Vulnerable Is Mega-Cap Tech To Tariff Turmoil? J.P. Morgan Asset Management, April 9th, 2025.

17) IBID.

18) BlackRock. Student of the Market. BlackRock, April 2025.

Important Information

The Clifford Group LLC (“The Clifford Group”) is a registered investment advisor. Advisory services are only offered to clients or prospective clients where The Clifford Group and its representatives are properly licensed or exempt from licensure. The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your attorney or tax advisor. The views expressed in this commentary are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur. All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability, or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. The information contained above is for illustrative purposes only.

For additional information, please visit our website at www.thecliffordgrp.com.

Risk Disclosure

Generally, among asset classes, stocks are more volatile than bonds or short-term instruments. Government bonds and corporate bonds have more moderate short-term price fluctuations than stocks, but provide lower potential long-term returns. U.S. Treasury Bills maintain a stable value if held to maturity, but returns are generally only slightly above the inflation rate. Risk associated with equity investing include stock values which may fluctuate in response to the activities of individual companies and general market and economic conditions. There are risks associated with investing in Real Assets and the Real Assets sector, including real estate, precious metals and natural resources. Investments can be significantly affected by events relating to these industries.