May Market Insights

Treasury Yields

Treasury yields have increased dramatically over the past three weeks, with the ten-year yield rising nearly half a percent to 4.613% and the thirty-year yield reaching 5.144%, its second-highest level in the last five years.

Treasury yields rise and fall based on the coupon set on the bond, which is the amount the federal government pays in interest, and the price paid to acquire the bond in the secondary market. When Treasury prices fall, yields rise. The Treasury issues new debt through auctions, where competitive bids determine the yield on newly issued bonds.

The recent movement in Treasury markets is being driven by several factors. Inflation fears in recent months, particularly since tariff discussions began, have pushed rates higher. Investors anticipating rising inflation and interest rates are less inclined to buy or hold Treasuries at current yields.¹ The market has also grown concerned about the size of the deficit and the prospect that it may widen further. Some estimates suggest that the tax bill passed by the House on Thursday morning will add approximately $275 billion to the deficit next year. While tariff revenues are expected to offset this increase, the package has still raised concerns that long-term debt sustainability is not being addressed, increasing perceived risk.² As a result, investors demand higher yields to compensate for that risk, pushing current Treasury prices down and their yields up.

On Friday, May 16, Moody’s became the third and final major credit rating agency to downgrade U.S. debt from Aaa to Aa1, the second-highest rating on its scale. While expected, given that Standard & Poor’s downgraded the U.S. in 2011 and Fitch followed in 2023, the move underscores lingering market anxiety over unresolved debt issues.³ The downgrade could also impact corporate credit ratings. According to the “sovereign ceiling rule,” no borrower within a country can have a higher credit rating than its government.⁴ This may slightly affect credit spreads, though company fundamentals remain the dominant factor.

On Wednesday, May 21, the U.S. Treasury auction saw weaker-than-average demand for new issuance.⁵ As noted above, auction yields are set by competitive bids. Softer demand leads to higher winning bids, which translates to higher yields in the secondary market.

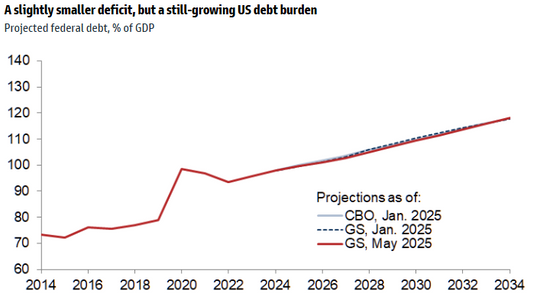

Source: Congressional Budget Office, Goldman Sachs Global Investment Research.6

Treasury yields are important for a number of reasons. Mortgage rates typically move in line with, but slightly above, the ten-year Treasury yield. With Treasury yields remaining elevated, mortgage rates are likely to stay high in the near term. In terms of the national debt, higher Treasury yields mean the federal government must spend more to service its debt. This doesn’t immediately increase the total debt, but it does raise borrowing costs over time. That, in turn, could contribute to larger future deficits and an increased debt-to-GDP ratio.

Economic Data

For several months, analysts have anticipated that tariffs would result in higher inflation readings. However, this expected increase in inflation has not yet materialized in a significant way. Last week’s headline CPI showed just a 0.2% month-over-month increase in prices, a relatively modest gain and below estimates.⁷ One explanation is that companies stockpiled inventories ahead of tariffs, easing price pressure. More importantly, producers appear to be absorbing some of the increased costs. The Producer Price Index fell 0.5% month over month in April, suggesting that firms are facing higher input costs but are holding off on price increases.⁸

On May 2, the Bureau of Labor Statistics reported that nonfarm payroll employment increased by 177,000 jobs in April, exceeding expectations and keeping the unemployment rate steady at 4.2%.⁹ This points to continued strength in the labor market.

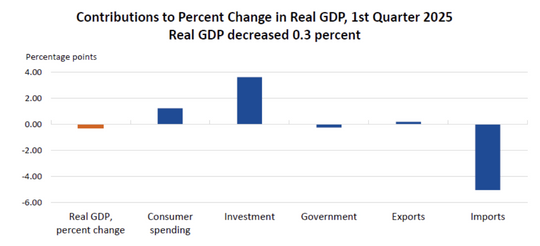

GDP in the first quarter decreased at an annualized rate of 0.3%.¹⁰ One silver lining is that the contraction was largely driven by a rise in imports, which subtract from GDP.¹¹ This increase likely reflects businesses moving up purchases to get ahead of tariffs and is expected to reverse direction in the next reading.

Source: U.S. Bureau of Economic Analysis. Imports are a subtraction in the calculation of GDP; thus, an increase in imports results in a negative contribution to GDP. Seasonally adjusted annual rates.12

The first-quarter corporate earnings season is nearly complete. If current pro forma estimates hold, earnings will show 13.4% year-over-year growth, though a -2.7% decline from the previous quarter.¹³ Despite the mixed results, 77% of companies reporting have exceeded estimates, with earnings coming in 10.3% above consensus.¹⁴ Altogether, corporate earnings have surprised to the upside and played a key role in the market’s recovery over the past month.

Given resilience in the jobs market and modest increases in inflation readings, the Fed’s decision on rates is likely to remain clouded. Chair Powell has remained steadfast in his focus on inflation reduction, and without weakness on the employment side, it is possible the FOMC will continue to hold off on any cuts in the absence of new information. The next FOMC announcement will come on June 18th.

Citations

1) Uruci, B. U.S. Economy At a Crossroads: Inflation, Trade Realignment, and the Road Ahead. T. Rowe Price, May 2025.

2) Grimberg, J. et al. What’s Top of Mind in Macro Research: Growing US Fiscal Concerns, Tracking Trade Flows, the Positives of Population Aging. Goldman Sachs, May 21, 2025.

3) Ibid.

4) Jackson, J. What are the implications of Moody’s Downgrade of the United States? J.P. Morgan Asset Management, May 21, 2025.

5) Goldfarb, S. Why Treasury Yields are Rising. The Wall Street Journal, May 21, 2025.

6) Grimberg, J. et al. What’s Top of Mind in Macro Research. Goldman Sachs, May 21, 2025.

7) J.P. Morgan Asset Management. Weekly Market Recap. May 19, 2025.

8) Ibid.

9) Bureau of Labor Statistics. The Employment Situation – April 2025. U.S. Department of Labor, May 2, 2025.

10) U.S. Bureau of Economic Analysis. Gross Domestic Product, 1st Quarter 2025 (Advance Estimate). U.S. Department of Commerce, April 30, 2025.

11) Ibid.

12) Ibid.

13) Kelly, D. Economic Update. J.P. Morgan Asset Management, May 19, 2025.

14) Ibid.

Important Information

The Clifford Group LLC (“The Clifford Group”) is a registered investment advisor. Advisory services are only offered to clients or prospective clients where The Clifford Group and its representatives are properly licensed or exempt from licensure. The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your attorney or tax advisor. The views expressed in this commentary are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur. All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability, or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. The information contained above is for illustrative purposes only.

For additional information, please visit our website at www.thecliffordgrp.com.

Risk Disclosure

No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. All investments include a risk of loss that clients should be prepared to bear. The principal risks of The Clifford Group strategies are disclosed in the publicly available Form ADV Part 2A. Although bonds generally present less short-term risk and volatility risk than stocks, bonds contain interest rate risks; the risk of issuer default; issuer credit risk; liquidity risk; and inflation risk.