June Market Insights

Resilience

Resilience has defined the U.S. economy in the second quarter of the year. Looking at year-to-date returns on major indices, it would be easy to forget that within the past 90 days, the S&P 500 entered correction territory, defined as a decline of 10 percent or more, and the Nasdaq Composite briefly fell into a bear market. These indices are now positive on the year. In fact, from their lows, both have entered a technical bull market. As of the close on Tuesday, June 10th, the S&P now sits just 1.8% below its all-time high, well within striking distance.

More important than the indices, however, is that this resilience has so far extended throughout the realm of economic hard data. The U.S labor market has remained strong to this point. Total non-farm payrolls increased by 139,000 jobs in May, and the unemployment rate once again remained at 4.2%.1 Average hourly earnings for employees rose by 0.4%.2 The Job Openings and Labor Turnover Survey (JOLTS) for April, released on June 9th, showed that job openings remained at 7.4 million and the job opening rate held at 4.4%.3 While layoffs did rise in April, the JOLTS numbers remain in-line with long-term averages.4 One area of relative weakening comes in the form of a soft data statistic, the labor market differential. This figure reflects the net percentage of survey respondents who say jobs are “plentiful” versus “hard to get.” As shown in the graph below, the differential has declined in recent months but remains positive.5 Throughout 2025, soft data has consistently trended more negative than hard data, with survey pessimism failing to materialize in any significant way in actual economic releases.

Source: Conference Board, J.P. Morgan Asset Management.6

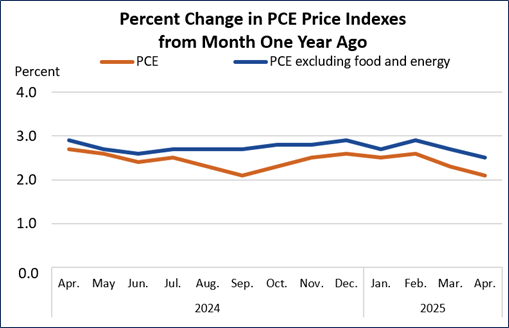

Consumer spending has also continued to increase. Personal Consumption Expenditures (PCE) rose by 0.2% in April.7 At the same time, Disposable Personal Income rose by 0.8%, indicating that while Americans are saving more than in prior months, consumer spending remains positive. The PCE Price Index, the Fed’s preferred inflation measure, decelerated in April to 2.1%, or 2.5% when excluding food and energy.8 Inflation is expected to tick up modestly as companies deplete pre-tariff inventories, but the current reading remains constructive.

Source: U.S. Bureau of Economic Analysis9

Two trends in the equity market have underscored the remarkable round trip we have seen so far this year. First, retail investors steadily and convincingly poured into the market in March and April. In March, retail investors set a record for the largest monthly retail inflow with $36 billion in net buys, only to raise that record in April with $40 billion.10 On April 29th, retail participation peaked at an all-time high, accounting for 36% of order flow.11 We view this as a positive sign aligned with strength in consumer spending. It also underscores a disconnect between consumer sentiment surveys and actual behavior. While soft data consumer sentiment declined over the same time frame, retail investors bet on long-term prosperity.12

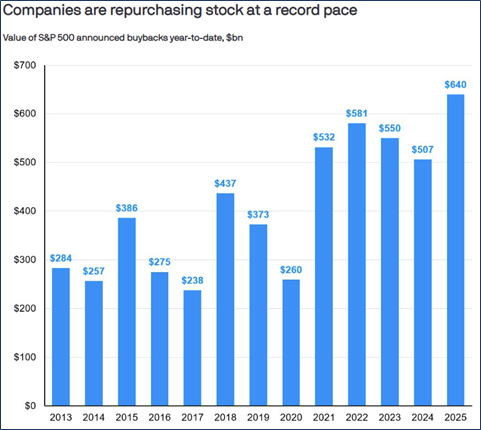

The second notable trend has been the high volume of corporate stock buybacks. As of June 4th, companies have bought back over $600 billion worth of their own stock this year.13 This puts 2025 on pace to exceed $1 trillion in total buybacks, a record.14 We interpret this as a signal that companies continue to forecast long-term earnings growth and are opportunistically taking advantage of short-term valuation dislocations.

Source: Bloomberg, S&P Global, J.P. Morgan Asset Management. Data is through May of each year. Data is as of May 30, 2025.15

Impacts from increased tariff levels to inflation and the labor market may still come, but resilience in the data to this point has underscored strength in the economy. In May, the NFIB Small Business Optimism Index rose by three points, moving above its 51-year average.16 Growing optimism among small business owners is a positive sign for the economy’s ability to withstand short-term volatility from top to bottom.

Upcoming Data and News to Watch

The May Consumer Price Index (CPI) report was released this morning and showed a 0.1% increase in May, a decrease from April’s 0.2% rise, placing the annual rate at 2.8%.17 President Trump announced this morning that a deal had been reached in principle with China on trade. While the full details are not yet known, it appears the deal will include the removal of some Chinese export controls on rare earth minerals.18 Finally, the FOMC will conclude its June meeting on June 18th. With steady employment numbers continuing, the FOMC may continue to hold rates at current levels.

Citations:

1. U.S. Bureau of Labor Statistics. Employment Situation Summary. U.S. Department of Labor, June 6th, 2025.

2. IBID.

3. U.S. Bureau of Labor Statistics. Job Openings, Hires, and Separations Little Changed in April 2025. U.S. Department of Labor, June 9th, 2025.

4. J.P Morgan Asset Management. Weekly Market Recap: Week of June 9, 2025. J.P. Morgan Asset Management, June 9th, 2025.

5. IBID.

6. IBID.

7. U.S. Bureau of Economic Analysis. Personal Income and Outlays, April 2025. U.S. Department of Commerce, May 30th, 2025.

8. IBID.

9. IBID.

10. Pandit, M. Who is buying U.S. Equities? J.P. Morgan Asset Management, June 4th, 2025.

11. IBID.

12. University of Michigan. Survey of Consumers. University of Michigan, May 30th, 2025.

13. Baccardax, M. Confidence Game: Share Buybacks Are Soaring. CEO Optimism Isn’t. Barron’s, June 4th, 2025.

14. IBID.

15. Pandit, M. Who is buying U.S. Equities? J.P. Morgan Asset Management, June 4th, 2025.

16. NFIB. New NFIB Survey: Small Business Optimism Increases in May. NFIB, June 10th, 2025.

17. U.S. Bureau of Labor Statistics. Consumer Price Index Summary. U.S. Department of Labor, June 11th, 2025.

18. Barnato, K. Trump Says ‘Deal with China is Done’ Over Restoring Trade Truce. The Wall Street Journal, June 11th, 2025.

Important Information

The Clifford Group LLC (“The Clifford Group”) is a registered investment advisor. Advisory services are only offered to clients or prospective clients where The Clifford Group and its representatives are properly licensed or exempt from licensure. The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your attorney or tax advisor. The views expressed in this commentary are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur. All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability, or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. The information contained above is for illustrative purposes only.

For additional information, please visit our website at www.thecliffordgrp.com.

Risk Disclosure

No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. All investments include a risk of loss that clients should be prepared to bear. The principal risks of The Clifford Group strategies are disclosed in the publicly available Form ADV Part 2A. Risk associated with equity investing include stock values which may fluctuate in response to the activities of individual companies and general market and economic conditions.