September Market Insights

Inflation, Employment, and the Fed’s Dual Mandate

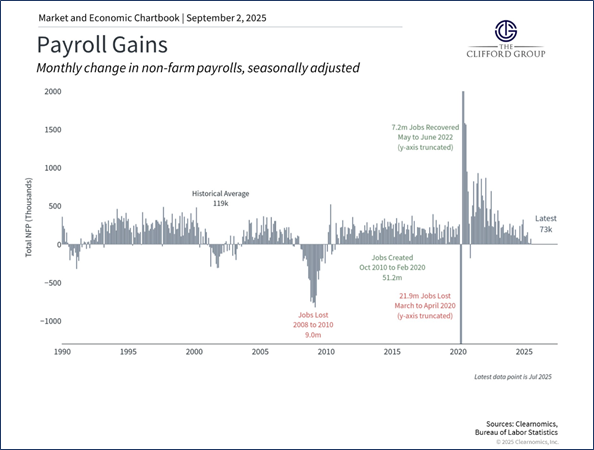

As the third quarter of 2025 nears its end, the Federal Reserve faces a highly anticipated yet uncertain decision on interest rates. The July nonfarm payrolls report showed a slowdown in job creation, with only 73,000 new jobs added and the unemployment rate unchanged.1 The bigger story, however, was the substantial downward revisions to May and June, which marked the first meaningful signal that labor market strength is waning. Taken together, the July data and the revisions suggest that job growth has been weaker for several months than previously believed.

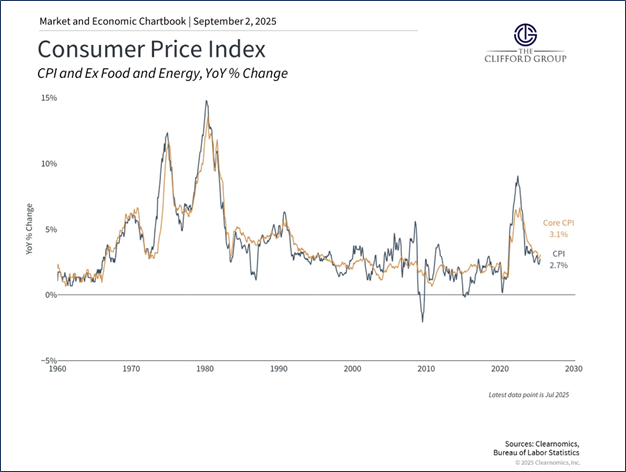

While employment numbers have softened, inflation is expected to increase modestly. Current estimates for the August CPI reading, which will be released on September 11th, suggest there could be a month-over-month increase of 0.4%. If realized, this would push the annual inflation measure back over 3%.2 This is a notable increase, and while most expectations are that inflation will remain relatively stable, the upward trend could make committing to any longer-term rate cutting cycle more difficult for the Fed.

Reduced immigration further adds to the complexity of the decision, as it may alter the pace of job creation needed to sustain wage growth.3 In this environment, a modest level of monthly job gains may represent the new equilibrium for the labor market.

In his speech on August 22nd at Jackson Hole, Chair Powell signaled that he was, at the very least, strongly considering a rate cut in the coming months.4 While the timing and the size of a cut remain to be seen, the market is now broadly anticipating a 25-basis point reduction in September.5 Expectations for further rate cuts after the September meeting have also risen in the wake of the July jobs report discussed above.6 Whether or not these cuts come to fruition will likely be heavily influenced by labor market readings that are yet to come. The August non-farm payrolls report from the Bureau of Labor Statistics is due out on Friday, September 5th, and will almost certainly play a large role in determining the Fed’s decision in September and beyond.

Earnings and Equity

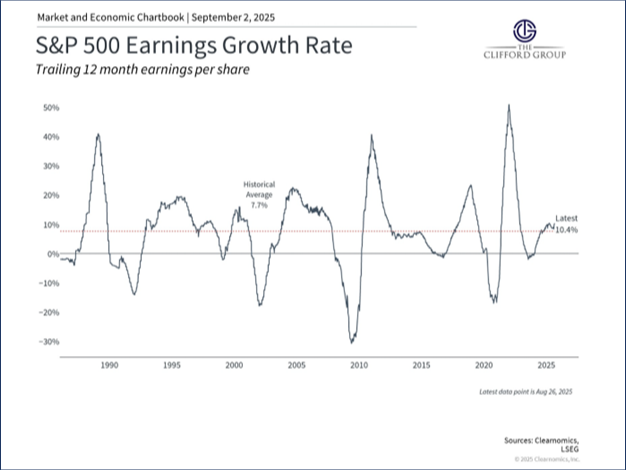

The second quarter earnings season is nearly complete, and, on the whole, earnings surprised to the upside by a considerable amount. Aggregate S&P 500 earnings per share grew by nearly 11% year over year, exceeding expectations by 7%.7 While this dramatic outperformance is in part due to the heavy slashing of estimates in the early part of the year, a firm positive side of earnings announcements was widespread upward revisions of corporate guidance and 2026 earnings estimates.8

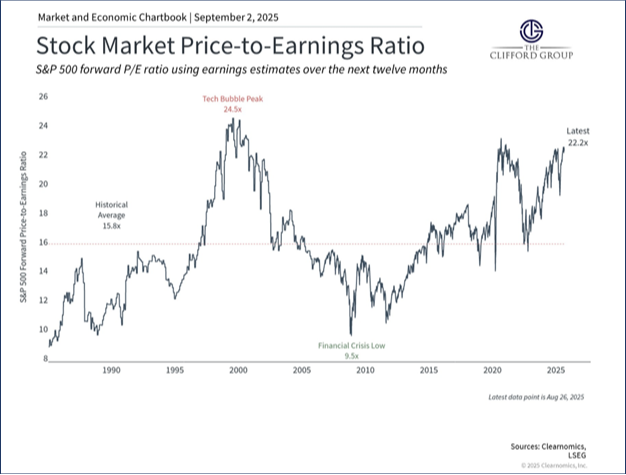

Strong performance through the summer accompanied these positive earnings. As a result, we now find ourselves in a market landscape where large cap price-to earnings ratios are once again highly elevated. The S&P 500 is trading at a forward P/E ratio over 22x, which is approximately 1.6 standard deviations above the 30-year average.9 The top-10 stocks in the S&P 500 now account for almost 40% of the index.10 While this market concentration presents a greater risk of volatility, as we saw in January of this year, second quarter earnings growth was still broad on a sector level. Of the 12 sectors in the index, 9 delivered positive year over year earnings per share growth.11

On Friday, August 29th, the Federal Court of Appeals ruled that the April 2nd reciprocal tariffs were not legal.12 The decision allows the tariffs to remain in place until October 14th to give the administration time to file an appeal with the U.S. Supreme Court. The tariffs rejected by the court account for approximately 70% of projected tariff revenue in 2026.13 While the market has reacted negatively to tariffs throughout 2025, the potential suspension of those tariffs did not drive an immediate rally. On Tuesday, September 2nd, intermediate and long-term bonds in the U.S experienced a small sell-off, which further influenced equity prices, in part due to concerns that the rejection of these tariffs by the court would increase future federal budget deficits.14

Private Equity Exits Up

A notable trend this year has been the sharp increase in private equity exit activity compared with the first half of 2024. Deal volume has risen 104% year over year, while deal count is up 18%.15 Exit opportunities were scarce in 2024, constrained by high interest rates and a weak IPO environment. Conditions have shifted: late-2024 rate cuts, ongoing expectations for further easing, and a healthier IPO market have all supported a rebound. First-half 2025 exits reached their second-highest volume on record.16 This is tremendously positive news for both fund managers and investors alike, who both depend on exits to create liquidity and generate real returns.

Important Information

The Clifford Group LLC (“The Clifford Group”) is a registered investment advisor. Advisory services are only offered to clients or prospective clients where The Clifford Group and its representatives are properly licensed or exempt from licensure. The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your attorney or tax advisor. The views expressed in this commentary are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur. All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability, or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. The information contained above is for illustrative purposes only.

For additional information, please visit our website at www.thecliffordgrp.com.

Risk Disclosure

No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment.

All investments include a risk of loss that clients should be prepared to bear. The principal risks of The Clifford Group strategies are disclosed in the publicly available Form ADV Part 2A.

Risk associated with equity investing include stock values which may fluctuate in response to the activities of individual companies and general market and economic conditions. Private funds (or other alternative investment funds) are designed only for sophisticated investors who are able to bear the risk of the loss of their entire investment. An investment in a private fund should be viewed as illiquid and interests in private funds are generally not readily marketable and are generally not transferable. Investors should be prepared to bear the financial risks of an investment in a private fund for an indefinite period of time. An investment in a private fund is not intended to be a complete investment program, but rather is intended for investment as part of a diversified investment portfolio. Typically interests in a private funds are not registered under the US Securities Act of 1933, as amended (“the Securities Act”), and the fund is not registered as an investment company under the US Investment Company Act of 1940, as amended (the “Investment Company Act”), and as such, investors will not be afforded the protections of those laws and regulations. A prospective investor should carefully review all offering materials associated with a private fund, including the risk factors, and should consult his or her own legal counsel and/or financial advisor prior to considering an investment in a private fund. Diversification does not ensure a profit or guarantee against loss. Although bonds generally present less short-term risk and volatility risk than stocks, bonds contain interest rate risks; the risk of issuer default; issuer credit risk; liquidity risk; and inflation risk.