August Market Insights

The Rhythm of the Market

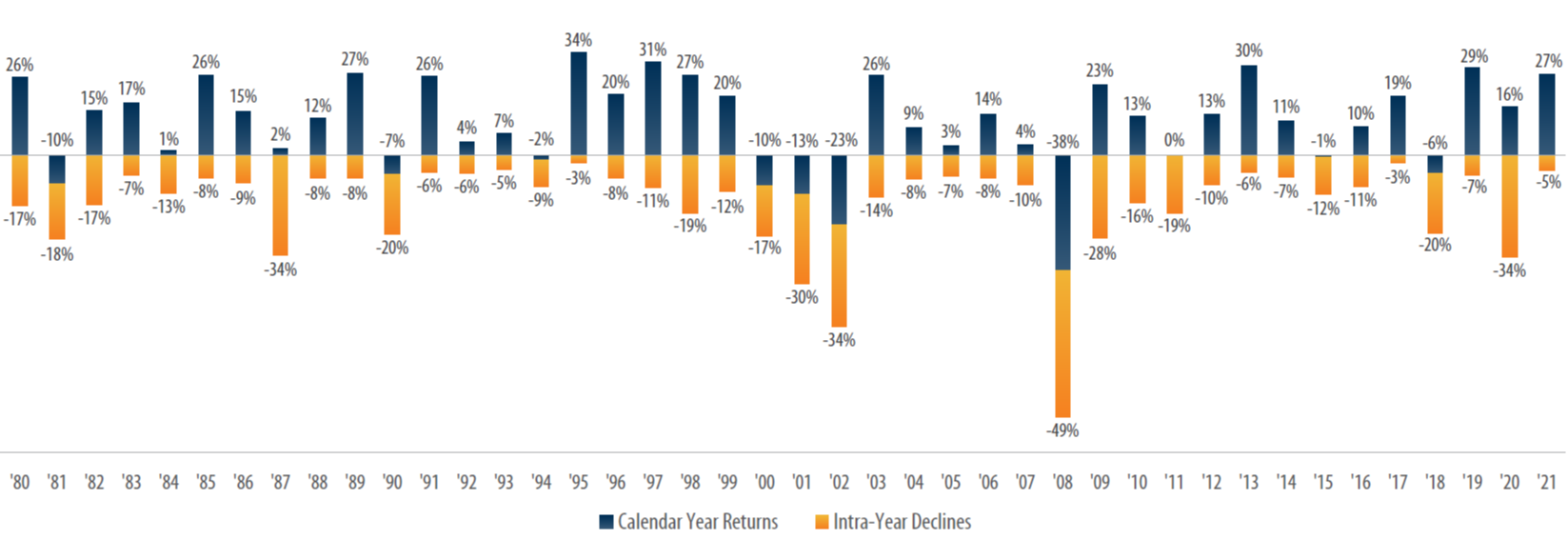

The past week’s negative price movement in the market represents two expected developments. First, a long-awaited tightening of growth was an unavoidable consequence of higher interest rates in the campaign to fight inflation. Second, experience shows that moderate pullbacks in the market happen a few times each year. Though short-term volatility dominates headlines, intra-year declines in the market are never the full story. As the graph below demonstrates, judging the market only by its worst days fails to capture the associated upside.1

Source: First Trust Portfolios; Benchmark: S&P 500 Index

GDP Growth

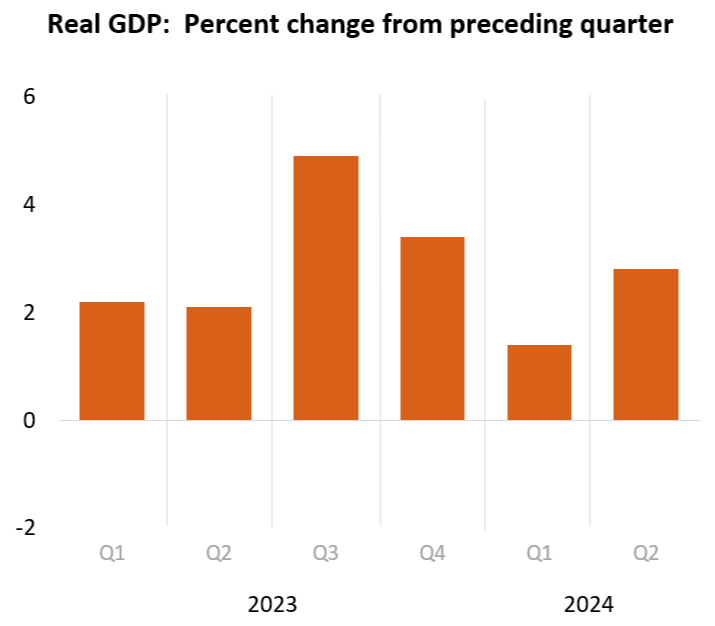

The second quarter has proven remarkably resilient when it comes to real GDP growth. The Q2 advance estimate projects that real GDP increased at an annual rate of 2.8%. This strong reading is a doubling of Q1’s real GDP and provides reason for optimism. Real GDP growth, because it accounts for inflation, demonstrates that production in the economy expanded, a positive sign for long-term national economic health.2

Source: U.S Bureau of Economic Analysis

Employment Report and Interest Rates

U.S hiring slowed more than expected in July, according to the Department of Labor’s monthly unemployment report published on August 2nd. The economy added a net 114,000 non-farm jobs and the unemployment rate rose to 4.3%, its highest level since 2021.3 While the labor market cool down was expected and even desired as an indicator that the Fed’s interest rate policy could begin easing, Friday’s higher-than-expected numbers created sentiment in the market that perhaps a rate cut is overdue. A September cut seems even more likely now. August’s unemployment report will likely play a large role in determining the size and frequency of interest rate cuts in the fourth quarter.4

There was positive news to come with the jobs report. Worker productivity rose at a pace of 2.7% from a year prior. This figure, 1.3% above the average year-over-year increase since 2009, could play a vital role in maintaining strong growth in the economy.5 Traditionally, as worker productivity rises and workers produce more with the same inputs, employers can increase wages without raising prices. Such a phenomenon creates real, non-inflationary, wage growth.6

Market Earnings Update

Despite more volatility than the first quarter’s earnings season, Q2 earnings reports have been mostly positive. The S&P 500 is reporting its highest year-over-year earnings growth rate since 2021. Of the S&P 500 companies that have reported earnings this quarter, 78% have surprised to the upside on earnings per share, beating both five and ten-year averages.7 Of the 611 companies in the Russell 2000 small cap index that have already reported their earnings, 75% have met or exceeded analyst EPS expectations.8 This serves to show that there is still wide spread growth throughout the economy. This growth was underscored on Monday by the Institute for Supply Management’s services-activity index release. July’s numbers outperformed June’s and beat analyst expectations. While this index does not carry quite the same weight as official job data, it is still a closely watched economic indicator.9

Finally, though headlines have focused on negative price performance in the Magnificent 7 following their earnings reports, much of the consternation in the market for these mega-caps has to do with impatience surrounding AI returns. While costs have certainly risen for these companies in the race for datacenters and chips to support AI development, fundamentals have remained strong as well.10

As earnings season continues, some volatility may remain. Despite this, plenty of reason for optimism can be found in GDP growth, worker productivity growth, and historical trends. A few bad days in the market never tell the full story.

Sources:

1) First Trust Portfolios. Staying the Course. First Trust Portfolios L.P. Accessed August 5, 2024.

2) U.S. Bureau of Economic Analysis, Gross Domestic Product. U.S Department of Commerce. Accessed August 5, 2024.

3) U.S. Bureau of Labor Statistics. Employment Situation Summary. U.S Department of Labor. August 2nd, 2024.

4) Hatzius, J. et al. USA: Payroll Growth Slows by More Than Expected. Goldman Sachs. August 2nd, 2024.

5) Lahart, J. Tight Job market Delivered Widespread Rewards. They Are at Risk. The Wall Street Journal. August 4, 2024.

6) Economic Strategy Group. In Brief: The Recent Rise in US Labor Productivity. The Aspen Institute. April 25, 2024.

7) Butters, J. S&P 500 Earnings Season Update: August 2, 2024. Factset. August 2, 2024.

8) Dhillon, T. Russell 2000 2024Q2 Earnings Dashboard. LSEG I/B/E/S. August 1, 2024.

9) Goldfarb, S. Stocks and Bond Yields Pare Decline After Solid Services Data. The Wall Street Journal. August 5, 2024.

10) Kolostyak, S. Magnificent 7 Stocks: US Tech Earnings in Full. Morningstar. August 5, 2024.

Important Information

The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your attorney or tax advisor. The views expressed in this commentary are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur. All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability, or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

Risk Disclosure

Generally, among asset classes, stocks are more volatile than bonds or short-term instruments. Government bonds and corporate bonds have more moderate short-term price fluctuations than stocks, but provide lower potential long-term returns. U.S. Treasury Bills maintain a stable value if held to maturity, but returns are generally only slightly above the inflation rate. Risk associated with equity investing include stock values which may fluctuate in response to the activities of individual companies and general market and economic conditions.