December Market Insights

The National Debt

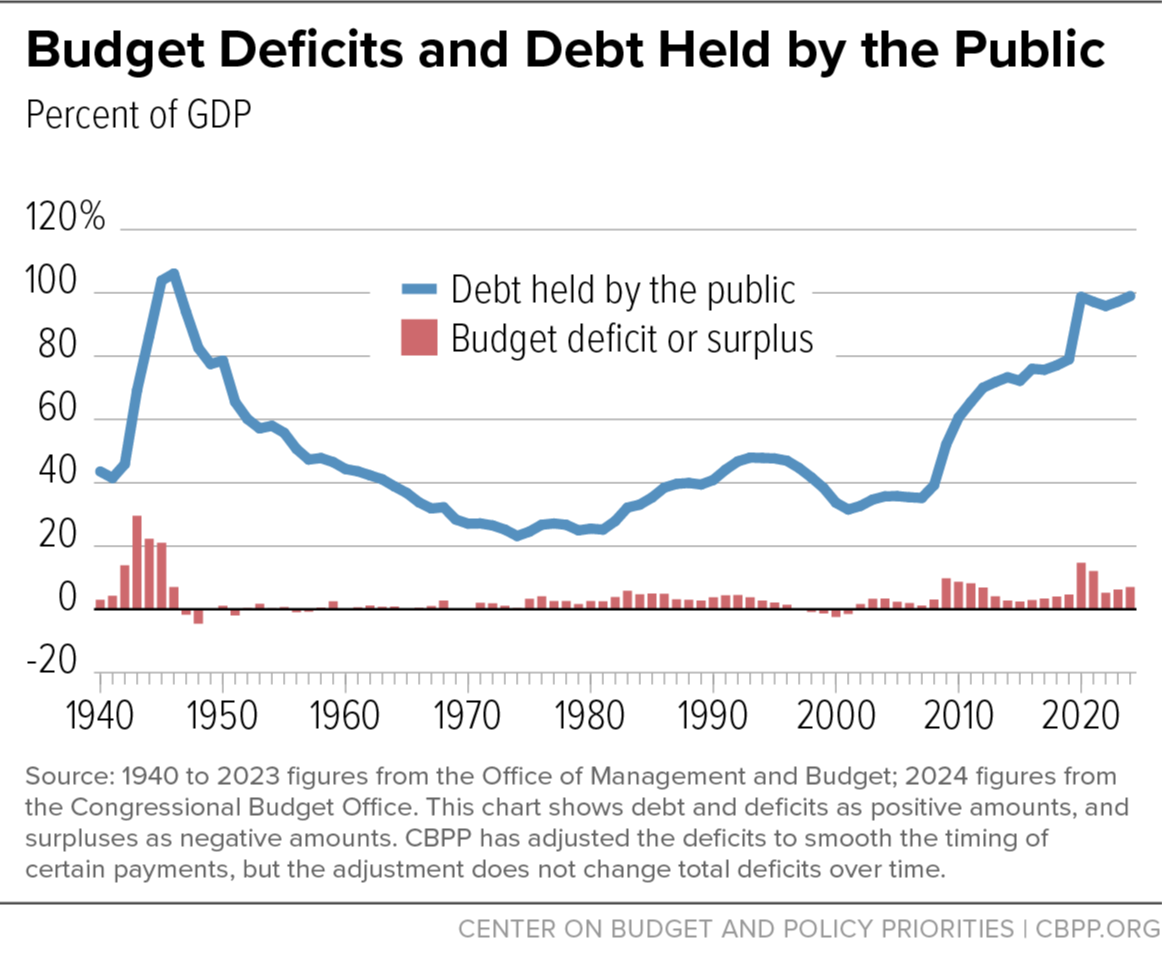

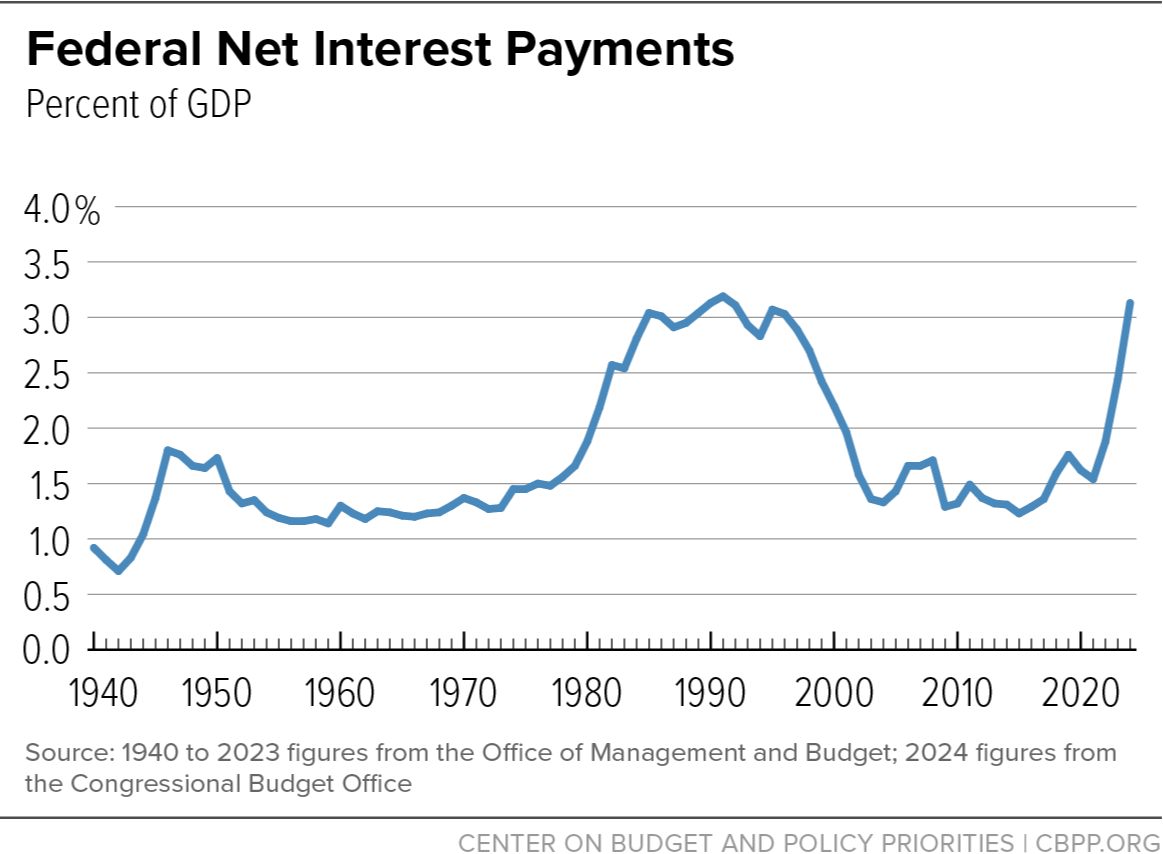

As of October 31st, the Federal debt held by the public was $28.57 trillion.1 This figure includes outstanding debt held by banks, private investors, and foreign governments. As can be seen in the graph below, debt held by the public, represented as a percentage of GDP, jumped in the wake of the 2008 Great Recession, and again in response to the Covid-19 pandemic. Current projections expect this debt metric to grow to 122% of GDP by 2034.2 Major contributors to the growing debt are sustained deficit spending and increases in required interest payments on the debt. This past fiscal year, federal deficit spending was $1.8 trillion dollars.3 In the context of higher for longer interest rates, servicing of the debt has grown as well. The Congressional Budget Office estimates that net interest payments in fiscal year 2024 rose to $949 billion.4 As the debt ratio rises, higher interest rates are also necessary to continue attracting lenders, which in turn makes future higher-debt levels even more expensive.

Source: Center on Budget and Policy Priorities.5

Growth in the long-term will, in and of itself, increase revenue streams for servicing the debt and funding spending. More significantly, sustained GDP growth would strenghten the debt ratio we discussed in the last paragraph, maintaining or reducing the interest rates necessary to entice lenders. Historically, the federal government has been able to balance crisis spending with positive growth in its aftermath, as was the case with WWII. In 1945, the Debt-GDP ratio grew to 106%. Strong economic performance spurred in part by labor force growth after the war contributed to a gradually reducing ratio that fell to less than 25% by 1974.6 While this example underscores the power of growth in righting the ship, our current conditions are not the same. Labor force growth today is much slower than it was during that time period as the baby boomer generation entered the workforce. While growth will be tremendously helpful in managing the national debt, it is unlikely to solve for it by itself.

Source: Center on Budget and Policy Priorities.7

Decreasing spending has received significant media attention over the last few weeks with President-elect Trump’s announcement of the Department of Government Efficiency. Meaningful spending cuts, combined with sustained economic growth and potential increases in revenue streams, may go a long way to stabilizing our debt levels in the medium to long term. Reducing the amount of new debt taken on, especially in a time when interest rates remain high and there is no necessity for crisis-level spending, could prove vital to the long-term economic health of the country.

US Economic Performance

The U.S economy looks to close out 2024 with 2.3% annual growth. Resilient consumer spending drove this number, contributing 78% of real GDP growth through the first three quarters of the year.8 Inflation-adjusted consumer spending grew 3.0% year over year in the third quarter, a 10% increase from the second quarter.9 While the November jobs report is yet to be released, unemployment to this point has held steady at 4.1%.10 These are all positive economic results and should give confidence in the state of the economy. On December 17 and 18, the Federal Open Markets Committee will meet to determine if there is going to be a final interest rate cut this year. While that decision is less certain than the past two, general opinion is that there will be a final 25 basis-point cut this year.11

These positive factors give us continued optimism that there are numerous opportunities to take advantage of as we move into the next year. U.S equities have outperformed the rest of the world throughout 2024 and current estimates are that they will do the same in 2025.12 With valuations currently at highs across growth stocks, we see continued opportunity in value stocks, mid- caps, and small-caps. While the Russell 1000 growth index is trading at a price-to-earnings (P/E) ratio of 32.8x, markedly above its 15-year average of 25.0x, the Russell 1000 value index is trading at 18.6x, just above its 15-year average.13 The last time similar gaps appeared in these ratios was December 2000; value stocks outperformed growth over the following one, three, and five year periods.14 The economic conditions continue to look positive for small and mid-cap stocks as well. As the Fed continues its spending cuts, the cost of growth for these smaller companies will continue to decline. Potential de-regulation in numerous industries under the next administration could potentially buoy companies in these size brackets as well.

Citations:

1. U.S Treasury Department. What is the national debt? FiscalData.Treasury.gov accessed December 3, 2024.

2. U.S Senate Subcommittee on the Budget. CBO: National Debt to Reach Record Share of GDP in Just Three Years. U.S Senate Subcommittee on the Budget, June 18, 2024.

3. Congressional Budget Office. Monthly Budget Review: Summary for Fiscal Year 2024. Congressional Budget Office, November 8, 2024.

4. IBID.

5. Center on Budget and Policy Priorities. Policy Basics: Deficits, Debt, and Interest. Center on Budget and Policy Priorities, November 20, 2024.

6. Gale, W and Rogers, T. Back to the Future: Can the Government Reduce Its Debt Again? Tax Policy Center, August 8, 2024.

7. Center on Budget and Policy Priorities. Policy Basics: Deficits, Debt, and Interest. Center on Budget and Policy Priorities, November 20, 2024.

8. Kelly, D and Aliaga, S. Economy: A post-cycle economy faces greater policy uncertainty. P. Morgan Asset Management, November 20, 2024.

9. IBID.

10. U.S Bureau of Labor Statistics. Employment Situation Summary. U.S Department of Labor, November 1, 2024.

11. Schneider, H. Fed’s Waller says he is inclined to cut rates in December. Reuters, December 2, 2024.

12. Li, W et al. Weekly Commentary. BlackRock, December 2, 2024.

13. Jacobs, J. Why Now May Be An Opportune Time For Active Value. BlackRock, November 21, 2024.

14. IBID.

Important Information

The Clifford Group LLC (“The Clifford Group”) is a registered investment advisor. Advisory services are only offered to clients or prospective clients where The Clifford Group and its representatives are properly licensed or exempt from licensure. The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your attorney or tax advisor. The views expressed in this commentary are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur. All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability, or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. The information contained above is for illustrative purposes only.

For additional information, please visit our website at www.thecliffordgrp.com.

Risk Disclosure

Risk associated with equity investing include stock values which may fluctuate in response to the activities of individual companies and general market and economic conditions. Investments in small-sized companies may involve greater risks than in those of larger, better known companies. Investments in mid-sized companies may involve greater risks than in those of larger, better known companies, but may be less volatile than investments in smaller companies.

Performance Disclosure

Past performance shown is not indicative of future results, which could differ substantially.