February Market Insights

In Like a Lion

The stock market experienced heightened volatility this month as investors weighed the potential impact of artificial intelligence on labor markets, sticky inflation, and rising geopolitical tensions.

Labor and AI

As the year has progressed, investor sentiment around artificial intelligence has swung from concerns that rapidly rising capital expenditures were unjustifiable to the opposite worry that AI-driven productivity gains could meaningfully disrupt labor markets in the short to intermediate term.

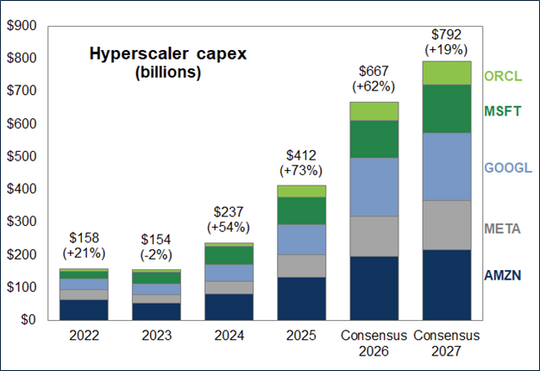

On February 4, Google released its Q4 2025 earnings report, showing strong performance across business segments. During the earnings call, the company announced plans to double capital expenditures in 2026 to $175 to $185 billion to support AI deployment.1 Despite strong growth and the fact that much of the spending will be directed toward meeting demand rather than pure research and development, Google shares came under pressure immediately following the announcement. This reaction largely reflected investor concern about the level of return required to justify such significant investment.

Just one day later, on February 5, OpenAI released GPT 5.3 Codex and Anthropic released Opus 4.6.2 Observers widely viewed these models as a meaningful step forward, particularly in agentic capabilities. In the weeks that followed, the market narrative shifted. Concern moved from whether AI investment would generate sufficient returns to whether the technology could become too productive for labor markets to adapt smoothly, potentially creating negative economic effects. Software companies also faced pressure amid speculation that AI agents could increasingly enable internal software development.3

On February 22, Alap Shah outlined a theoretical chain of negative outcomes from AI automation in a piece that quickly went viral and contributed to market weakness.4 Concerns intensified further when fintech company Block and CEO Jack Dorsey announced plans to lay off roughly half of the workforce while increasing automation.5

Source: FactSet, Goldman Sachs Global Investment Research.

We believe the initial concerns about AI investment returns were overly broad. Some companies will capture meaningful value, while others may lag. Overall, we continue to view AI-driven productivity gains as a structural tailwind for hyperscalers, AI infrastructure providers, and diversified end users that adopt the technology effectively. While clearly quantified benefits have been limited in earnings calls so far, analysts expect companies to begin identifying measurable returns more clearly in 2026.6

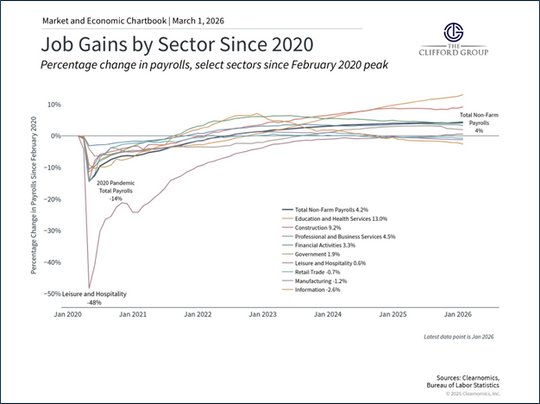

The labor market impact remains an important area of debate. Disruption over the intermediate to long term appears likely, but the level of anxiety seen in recent weeks does not represent the base case. Current estimates suggest only about 2.5% of U.S. jobs are exposed to automation today.7 Analysts currently expect AI to reduce annual hiring by roughly one million jobs and displace about 6 to 7% of the workforce over an extended period. The U.S. economy, however, creates approximately 30 million gross new jobs each year, largely driven by technological change, implying meaningful capacity to absorb disruption of this magnitude.8 This is especially relevant given the continued relative strength of the labor market.

Regardless of the precise pace of labor disruption, we believe the most effective way to capture AI-driven growth remains broad equity ownership across the AI ecosystem, including hyperscalers, their suppliers, and diversified end users positioned to benefit from productivity gains.

Source: Clearnomics, Bureau of Labor Statistics.

Iran

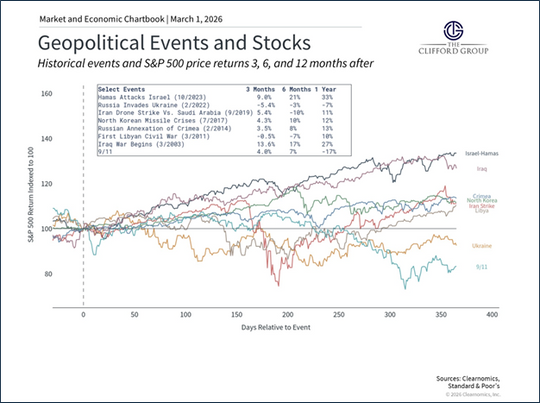

On Saturday morning, the United States and Israel began joint combat operations in Iran. While current indications suggest U.S. involvement will be primarily limited to airstrikes, the ultimate duration of the conflict remains uncertain. In an interview Sunday, President Trump said the operation could take “four weeks or less.”9

The most immediate market sensitivity is energy. On Sunday, Iran began restricting traffic through the Straight of Hormuz, a passage through which approximately 20% of the global supply of oil and liquefied natural gas travels, by engaging ships in the area. As of Sunday evening, more than 200 ships that intended to traverse the straight had dropped their anchors in the surrounding waters while the situation developed.10 Over the weekend, retail oil prices rose by approximately 15% while liquefied natural gas prices had not yet fully adjusted but appear likely to respond early in the trading week.11

The most critical factor for energy prices will be the duration of the straight’s closure. While current traffic is slowed, oil prices were already depressed. If the current baseline of a four-to-six-week closure holds, prices should remain within historical norms.12 This fluctuation in energy prices along with the uncertainty at the center of the conflict will likely increase volatility in the coming days.

Source: Clearnomics, Standard & Poor’s.

Citations:

1. Mickle, T. Google Plans to Double Spending Amid A.I Race. The New York Times, February 4th, 2026.

2. Shumer, M. Something Big is Happening. Shumer, Matt, February 9th, 2026.

3. Aliaga, S and Cangialosi, N. What does AI disruption mean for investors? J.P. Morgan Asset Management, February 20th, 2026.

4. Shah, A. The 2028 Global Intelligence Crisis. Citrini Research, February 22nd, 2026.

5. Cutter, C. The Week the Dreaded AI Jobs Wipeout Got Real. The Wall Street Journal, February 28th, 2026.

6. Hammond, R et al. The Broadening of the AI Trade. Goldman Sachs, February 24th, 2024.

7. Briggs, J. Q&A on AI Labor Market Disruption. Goldman Sach, February 27th, 2026.

8. IBID.

9. Reals, T. et al. Trump says Iran operation could take “four weeks or less,” 3 U.S. troops killed. CBS News, March 1st, 2026.

10. Saba, Y. et al. Three tankers damaged in Gulf and one seafarer killed as US-Iran conflict escalates. Reuters, March 1st, 2026.

11. Struyven, D. et al. The Risk to Energy Prices from Iran. Goldman Sachs, March 1st, 2026.

12. Elliott, R. Oil Prices Climb After Iran Attack, Pointing to Economic Risks. The New York Times, March 1st, 2026.

13. Wilson, D. et al. Global Markets Comment: Market Thoughts Following the Strikes in Iran. Goldman Sachs, March 1st, 2026.

Important Information

The Clifford Group LLC (“The Clifford Group”) is a registered investment advisor. Advisory services are only offered to clients or prospective clients where The Clifford Group and its representatives are properly licensed or exempt from licensure. The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your attorney or tax advisor. The views expressed in this commentary are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur. All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability, or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. The information contained above is for illustrative purposes only. The above targets are estimates based on certain assumptions and analysis made by the advisor. There is no guarantee that the estimates will be achieved.

For additional information, please visit our website at

www.thecliffordgrp.com.