January Market Insights

Economy

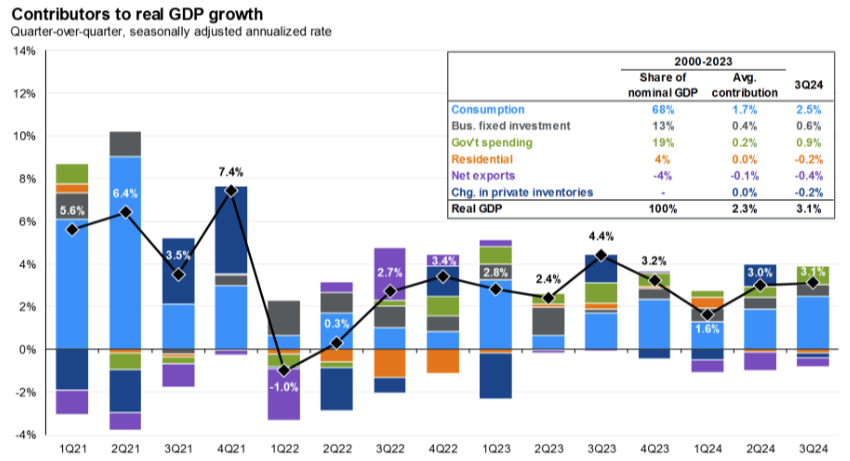

The economy closed out the year on sound footing. The U.S added 227,000 non-farm jobs to payrolls in November and the unemployment rate stayed put at 4.2%.1 The December employment report will be released this Friday and current projections expect that 160,000 non-farm jobs were added to payrolls.2 According to the third estimate, real gross domestic product grew by 3.1% annually in the third quarter of 2024.3 This was driven, in large part, by a 3.7% growth in consumer spending and a 4.0% increase in business fixed investment.4 These numbers are strong indicators that the economy is healthy and remains primed for continued growth.

Source: J.P. Morgan Asset Management, Guide to the Markets.5

On the markets side, third quarter earnings per share grew by 4.6% year-over-year and 1.8% quarter-over-quarter.6 While tech stocks continued to perform, healthcare led the charge as well with double digit earnings growth. Regulation roll backs and lower interest rates over the course of the next year appear to prime manufacturing related sectors and financials for growth in the near-term.7 Projections for U.S equities as a whole continue to outpace foreign markets. Current estimates for 12-month earnings growth place U.S companies more than 10% ahead of the nearest foreign market.8 While there is significant discussion throughout the industry about current valuation levels of large cap companies, the statistics are largely skewed by the top heavy performers from the past two years. When you exclude the top 10 companies in the United States, as measured by market cap, price to earnings ratios are much closer to the market average since 1996.9 While small cap companies stumbled in the closing months of 2024, forward looking projections for 2025 earnings expect tremendous growth for small caps as one of the main beneficiaries of reduced regulation and lower interest rates.10 These facts continue to lend support to the argument that we will see a broadening of performance across sectors in 2025.

Small Businesses

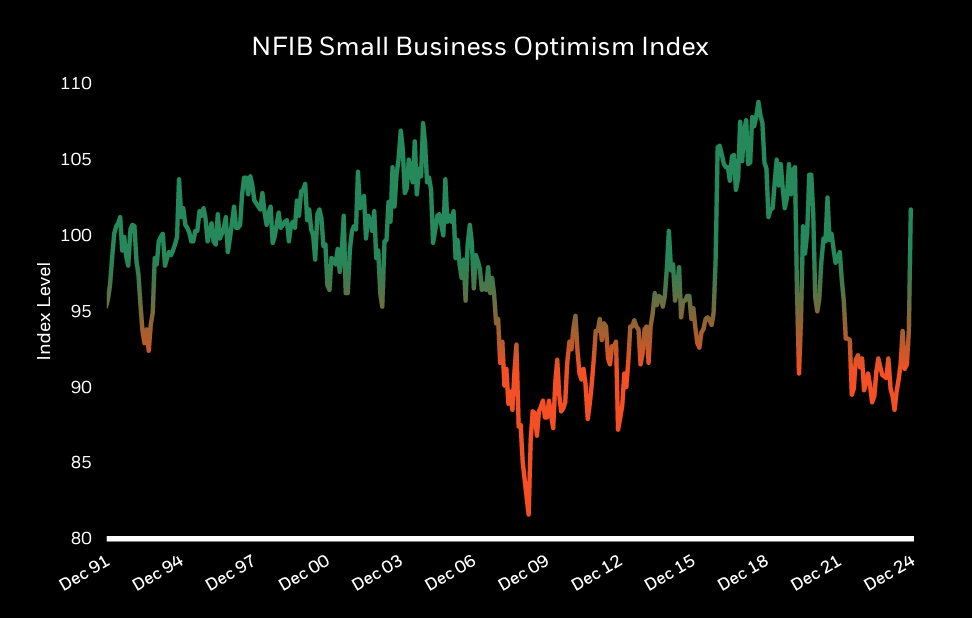

On a similarly positive note, the NFIB Small Business Optimism Index turned positive for the first time since the Covid-19 pandemic. Small business owners that were waiting for volatile moments like the 2024 Presidential Election to pass have begun investing at multi-year highs over the past 2 months.11

Source: BlackRock, On Target.12

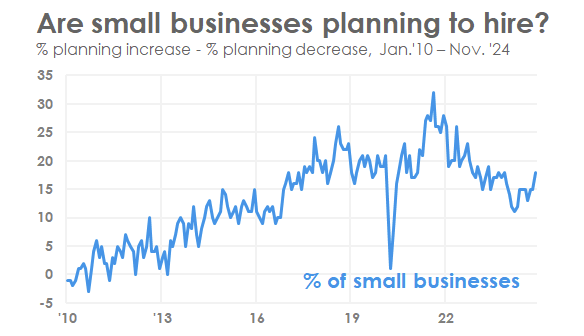

In November 2024, 18% of small business owners reported that they planned to create new jobs in the next three months, up 3 points from October’s NFIB survey.13 This not only points to an increase in economic activity for small businesses, but also indicates that a previously lagging source of hiring within the economy could grow in scale through 2025.

Source: National Federation of Independent Business, Jobs Report.14

Citations:

1) Bureau of Labor Statistics. The Employment Situation- November 2024. U.S. Department of Labor, December 6, 2024.

2) Golle, V. and Stirling, C. December US Jobs Report to Cap Year of Moderate Hiring. Bloomberg, January 4, 2025.

3) Bureau of Economic Analysis. Gross Domestic Product (Third Estimate), Corporate Profits (Revised Estimate), and GDP by Industry, Third Quarter 2024. U.S Department of Commerce, December 19, 2024.

4) J.P. Morgan Asset Management. Economic Update: Week of January 6, 2025. J.P. Morgan Asset Management, January 6, 2025.

5) Kelly, D. et al. Guide to the Markets. J.P. Morgan Asset Management, December 31, 2024.

6) J.P. Morgan Asset Management. Economic Update: Week of January 6, 2025. J.P. Morgan Asset Management, January 6, 2025.

7) IBID.

8) Kelly, D. et al. Guide to the Markets. J.P. Morgan Asset Management, December 31, 2024.

9) IBID.

10) IBID.

11) Gates, M. et al. On Target: Target Allocation ETF Model Portfolios Monthly market and portfolio insights December 2024. BlackRock, December 31, 2024.

12) IBID.

13) National Federation of Independent Business. Jobs Report. December 10, 2024.

14) IBID.

Important Information

The Clifford Group LLC (“The Clifford Group”) is a registered investment advisor. Advisory services are only offered to clients or prospective clients where The Clifford Group and its representatives are properly licensed or exempt from licensure. The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your attorney or tax advisor. The views expressed in this commentary are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur. All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability, or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. The information contained above is for illustrative purposes only.

For additional information, please visit our website at www.thecliffordgrp.com.

Risk Disclosure

Generally, among asset classes, stocks are more volatile than bonds or short-term instruments. Government bonds and corporate bonds have more moderate short-term price fluctuations than stocks, but provide lower potential long-term returns. U.S. Treasury Bills maintain a stable value if held to maturity, but returns are generally only slightly above the inflation rate. Risk associated with equity investing include stock values which may fluctuate in response to the activities of individual companies and general market and economic conditions. Investments in small-sized companies may involve greater risks than in those of larger, better known companies.