January Market Insights

The 2026 Starting Point

The start of the new year presents several notable market narratives. In 2025, the U.S. economy demonstrated resilience alongside strong market performance, despite a backdrop of geopolitical developments that many expected to constrain growth. Consumer sentiment, as measured by the University of Michigan survey, remains weaker than it has been 96 percent of the time since 1978.¹ As we have discussed previously, this measure continues to provide a distorted view of underlying economic conditions. The “misery index”, which combines the unemployment rate and CPI inflation to assess actual economic pressure on households rather than perceived sentiment, currently stands better than it has 76 percent of the time over the past 50 years.²

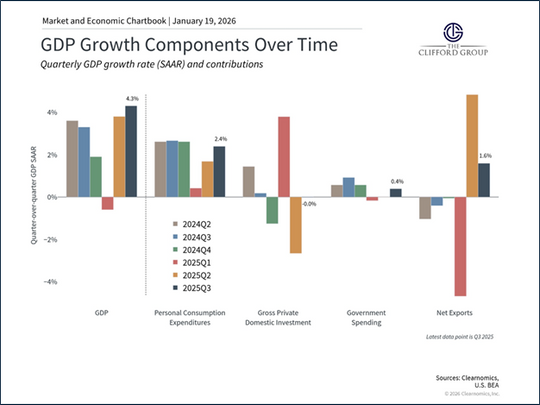

Real GDP growth for the fourth quarter of 2025 relative to the fourth quarter of 2024 is expected to be just under 2.5 percent.³ This outcome would exceed consensus expectations from the start of the year and materially outperform the revised forecasts issued following tariff announcements.⁴

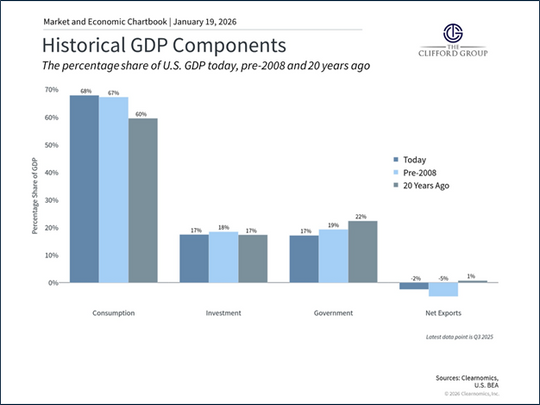

In the third quarter of 2025, the most recent period for which GDP component data are available, personal consumption remained the primary driver of economic growth.⁵ Government spending made a positive contribution after two consecutive quarters of decline, while net exports continued to support overall growth.⁶ We view the sustained strength of personal consumption as a constructive signal for ongoing economic stability.

Gold and Liquid Gold

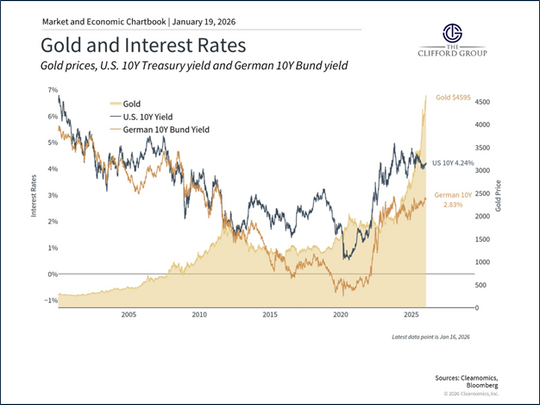

Gold prices rose sharply in 2025, surpassing $4,000 per ounce for the first time in October.⁷ During the third quarter of 2025, investor demand for gold was more than 50 percent higher by tonnage than the average of the prior four quarters.⁸ This elevated demand reflects several factors that are likely to persist, at least in part, into 2026. Gold is commonly viewed as a hedge against inflation, currency depreciation, and geopolitical uncertainty, and investors increased allocations for these reasons throughout 2025.

At the same time, central banks materially expanded their gold reserves. In November alone, central banks purchased 45 tons of gold, bringing total purchases for 2025 to 297 tons.⁹ Forecasts suggest that China and other emerging market central banks will continue accumulating gold in the coming year as protection against geopolitical and sanction-related risks.¹⁰

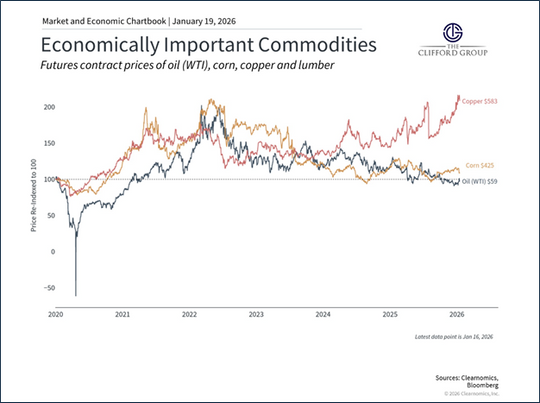

While gold delivered strong performance in 2025, oil prices declined amid ample global supply. Continued production growth in the United States and Russia, along with the potential for increased output from Venezuela, has led analysts to project further downside pressure in 2026.¹¹ Price volatility could still emerge from geopolitical developments, particularly as major producers such as Iran and Russia remain subject to sanctions that appear more likely to intensify than to ease. Signs of this risk have already surfaced, with oil prices rising over the past two weeks as political unrest in Iran increased the possibility of supply disruptions.¹²

Recently, however, geopolitically driven price spikes have been short lived. Sustained lower gasoline prices have provided a meaningful benefit to U.S. consumers, supporting household balance sheets. We expect this dynamic to continue and to help offset the impact of inflation should price pressures reaccelerate.

Citations

1) Dr. Kelly, D. A Baseline Forecast for 2026.J.P. Morgan Asset Management, January 5th, 2026.

2) IBID.

3) Walker, R. Economic Data Surprises, Our Forecast Performance, and Market Reactions in 2025. Goldman Sachs, January 17th, 2026.

4) IBID.

5) Bureau of Economic Activity. Gross Domestic Product, 3rd Quarter 2025 (Initial Estimate) and Corporate Profits (Preliminary). U.S. Department of Commerce, December 23rd, 2025.

6) IBID.

7) J.P. Morgan Asset Management. Will Gold Prices Break $5,000/oz in 2026? J.P. Morgan Asset Management, December 16th, 2025.

8) IBID.

9) Salim, M. Central Bank Gold Statistics: Buying Momentum Continues Into November. World Gold Council, January 6th, 2026.

10) Struyven, D. et al. 2026 Outlook: Ride the Power Race and Supply Waves. Goldman Sachs, December 18th, 2025.

11) Struyven, D. et al. 2026 Outlook: Prices Trend Down on Strong Supply; Geopolitical Risks Remain. Goldman Sachs, January 11th, 2026.

12) Grigsby, Y. et al. Oil Comment: Market Pricing of Iran and Venezuela Shocks [Corrected]. Goldman Sachs, January 14, 2026.

Important Information

The Clifford Group LLC (“The Clifford Group”) is a registered investment advisor. Advisory services are only offered to clients or prospective clients where The Clifford Group and its representatives are properly licensed or exempt from licensure. The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your attorney or tax advisor. The views expressed in this commentary are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur. All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability, or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. The information contained above is for illustrative purposes only.

For additional information, please visit our website at www.thecliffordgrp.com.

Risk Disclosure

No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. All investments include a risk of loss that clients should be prepared to bear. The principal risks of The Clifford Group strategies are disclosed in the publicly available Form ADV Part 2A. Investing in commodities entails significant risk and is not appropriate for all investors. The major risks associated with investing in the natural resources sector, including large price volatility due to non-diversification and concentration in natural resources companies. There are risks associated with investing in Real Assets and the Real Assets sector, including real estate, precious metals and natural resources. Investments can be significantly affected by events relating to these industries.