Ongoing Conflict

The ongoing conflict in Iran has been the primary driver of recent market volatility and will likely remain so until the core risks associated with the situation are resolved. Within the conflict itself, we appear to be approaching a significant inflection point. On Saturday, President Trump issued an ultimatum to the Iranian regime, stating that if the Strait of Hormuz was not reopened by Monday, the United States would target Iranian energy infrastructure.¹ This threat placed downward pressure on futures markets over the weekend.

On Monday morning, however, the President announced an extension of the deadline to allow negotiations to continue. These discussions began over the weekend after several Gulf nations opened dialogue with the Islamic Revolutionary Guard Corps.² As they have since the beginning of the conflict, market participants have reacted sharply in both directions to each new and often contradictory headline.

The United States proposed a 15-point plan offering significant sanctions relief and support for a civilian nuclear power program in exchange for the forfeiture of Iran’s enriched uranium, the cessation of its nuclear weapons program, and limitations on ballistic missile development, among other provisions.³ On Wednesday, Iran appeared to reject the proposal.⁴ At the same time, the United States currently has more than 2,000 Marines capable of conducting amphibious operations deploying to the region. On Tuesday, it was announced that over 3,000 soldiers from the Army’s 82nd Airborne Division would be sent as well.⁵ Both forces are expected to arrive in the region by Friday.

As of Tuesday, the United States was awaiting a response from Tehran regarding participation in formal peace talks that could begin as early as Thursday. ⁶ The arrival of additional U.S. military assets in the region at roughly the same time as the President’s extended deadline suggests that we are approaching this inflection point sooner rather than later.

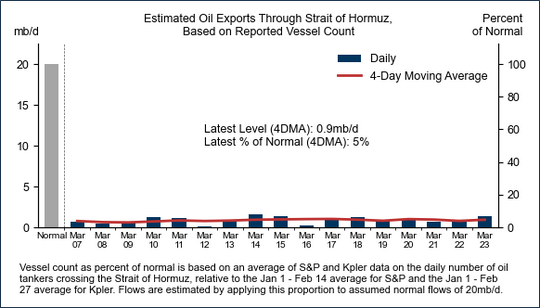

Source: S&P Global Commodities at Sea, Kpler, Goldman Sachs Global Investment Research

Iran’s primary response has been the closure of the Strait of Hormuz, which has driven oil prices higher. Rising energy prices have pressured equity markets globally and will likely contribute to higher inflation readings in the coming months. Current baseline expectations suggest U.S. headline inflation, which includes energy prices, could increase by approximately 0.8 percent over the next one to two months.⁷ Core inflation, which excludes standalone energy prices, is expected to rise much more modestly, in the range of 0.10 to 0.13 percent.⁸

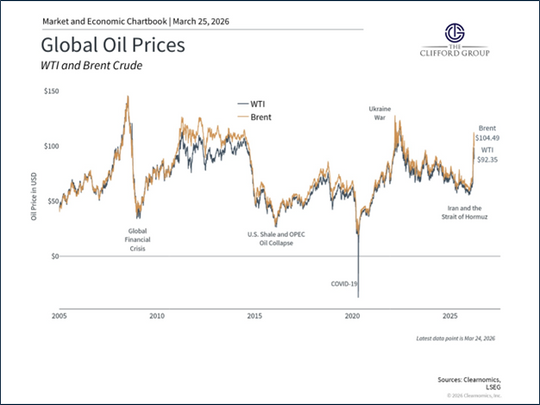

Source: Clearnomics, LSEG.

What does this mean for markets and the economy?

While the market volatility of the past month has been uncomfortable, we believe it has not eroded the fundamental factors driving economic strength and market performance. Chief among these factors is continued earnings outperformance. Current forecasts call for robust growth, with S&P 500 earnings expected to rise by 20 percent over the next twelve months.⁹

Importantly, even as market prices declined, analysts have continued to raise profitability estimates. Before the conflict began, S&P 500 companies were expected to grow profits by 10.9 percent in the three months through March. That estimate has since increased to 11.9 percent.¹⁰ We view this as a very positive signal, with valuations and entry points resetting to lower levels without deterioration in one of the key drivers of growth. At the beginning of the week, the S&P 500 traded at a next-twelve-months price-to-earnings ratio of 19.7, an attractive level relative to recent years.¹¹

Source: Clearnomics, LSEG.

Although higher energy prices will likely generate inflation-related headlines over the next two months, the medium-term inflation outlook remains constructive. Current estimates suggest core PCE inflation could be approximately 2.5 percent at year-end.¹² While this estimate has increased since the conflict began, it still implies roughly 50 basis points of disinflation from current levels.

Given near-term upward pressure on prices, the Federal Reserve appears unlikely to cut the federal funds rate at its April meeting. This stance is understandable in the present context. However, continued easing in inflation beyond the immediate term should give policymakers ample flexibility to manage rates in line with both sides of their dual mandate, labor and inflation.

The situation in the Middle East has dominated market price movements over the past month, but we expect this influence to diminish in the near future. To date, developments in Iran have not altered the underlying themes that support our optimism for sustained market performance. Earnings continue to grow and exceed expectations. Artificial intelligence and other technological advances are improving worker productivity and supporting robust spending. In the post-2022 market environment, valuations remain attractive.

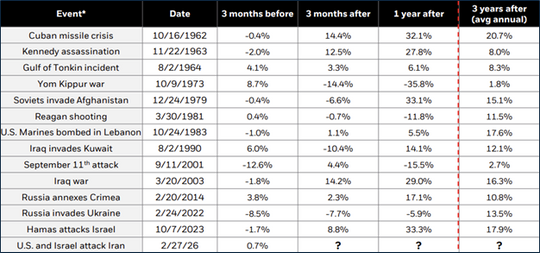

Finally, it is important to remember that geopolitical events typically do not dictate market performance beyond their immediate aftermath. Of the 14 significant geopolitical events shown below, markets were higher one year later in 10 instances. In the four cases with negative one-year returns, outcomes were driven by structural economic conditions unrelated to geopolitics, including high inflation and interest rate hikes in 2022, the aftermath of the dot-com bubble in 2001, tight monetary policy in the early 1980s, and stagflation in 1973. In every case, markets delivered positive annualized returns over the subsequent three-year period.

Source: BlackRock

Citations:

- Said, S. et al. The Back-Channel Diplomacy Behind Trump’s U-Turn on Iran.The Wall Street Journal, March 23rd, 2026.

- IBID.

- Miller, G. et al.U.S. plan to end war seeks removal of Iran’s enriched uranium, officials say.The Washington Post, May 25th, 2026.

- Faucon, B. and Kivilcim, E.Iran Rejects U.S. Proposal to End the War, Wants Reparations and Control of Hormuz.The Wall Street Journal, May 25th, 2025.

- Seligman, L et al. Pentagon to Order 3,000 82nd Airborne Soldiers to Middle East.The Wall Street Journal, March 24th, 2025.

- Fassihi, F. et al. Iranians reject Trump’s offer for a cease-fire but signal openness to talk. The New York Times, March 25th, 2026.

- Hatzius, J. Global Views: Brent or Broken? Goldman Sachs, March 23rd, 2026.

- IBID.

- Semenova, A. and Griffin, M. Morgan Stanley’s Wilson Sees S&P Profit Boom Despite Iran War. Bloomberg, March 25th, 2025.

- IBID.

- J.P. Morgan Asset Management.Weekly Market Recap.J.P. Morgan Asset Management, March 23, 2026.

- Hatzius, J. Global Views: Brent or Broken? Goldman Sachs, March 23rd, 2026.

Important Information

The Clifford Group LLC (“The Clifford Group”) is a registered investment advisor. Advisory services are only offered to clients or prospective clients where The Clifford Group and its representatives are properly licensed or exempt from licensure. The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your attorney or tax advisor. The views expressed in this commentary are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur. All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability, or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

The information contained above is for illustrative purposes only.

For additional information, please visit our website at www.thecliffordgrp.com.

Risk Disclosure

No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment.

All investments include a risk of loss that clients should be prepared to bear. The principal risks of The Clifford Group strategies are disclosed in the publicly available Form ADV Part 2A.

Diversification does not ensure a profit or guarantee against loss. Risk associated with equity investing include stock values which may fluctuate in response to the activities of individual companies and general market and economic conditions. The major risks associated with investing in the natural resources sector, including large price volatility due to non-diversification and concentration in natural resources companies.

Performance Disclosure

Index returns are unmanaged and do not reflect the deduction of any fees or expenses. Index returns reflect all items of income, gain and loss and the reinvestment of dividends and other income. You cannot invest directly in an Index.

For additional information, please visit our website at

www.thecliffordgrp.com.