November Market Insights

Election

As it currently stands, Republicans appear to be headed for a sweep of the Presidency, Senate, and House of Representatives. Donald Trump was elected the 47th President of the United States on Tuesday night and Republicans gained control of the Senate. Though votes in House races are still being counted as of Wednesday afternoon, Republicans appear likely to retain control there as well. Assuming that the House of Representatives outcome is as expected, there are several economic trends that are beginning to come into focus.

With a unified Republican government, a full extension of the Tax Cuts and Jobs Act of 2017, which would otherwise expire at the end of 2025, is very probable. This may also include a reinstatement of business investment incentives that have already expired.1

Implementation of tariffs on imported goods from China and potentially certain sectors, such as automobiles, from the European market will also likely be implemented quickly after the inauguration. While estimates vary, the market currently suggests these tariffs could land somewhere in the neighborhood of an additional 20% to 60% on imports from China. On the lower end of the spectrum, a 20% tariff on Chinese goods may push consumer prices up by approximately 0.30%.2 Should tariffs land at 60% on Chinese goods and 10% on goods from everywhere else, as was discussed during the campaign, current estimates expect a roughly 0.9% one-time increase in consumer prices.3 In essence, there may be an upward pressure on inflation at the outset of tariffs that should return to the underlying trend in the long-run.

Expectations that the Trump administration will ease regulation on businesses have been a source of positive movement in the market. Financials and small caps have seen the largest gains because of this. Generally speaking, regulation affects small cap companies in an outsized manor and reducing regulation may give these companies room to grow.4

Earnings Season

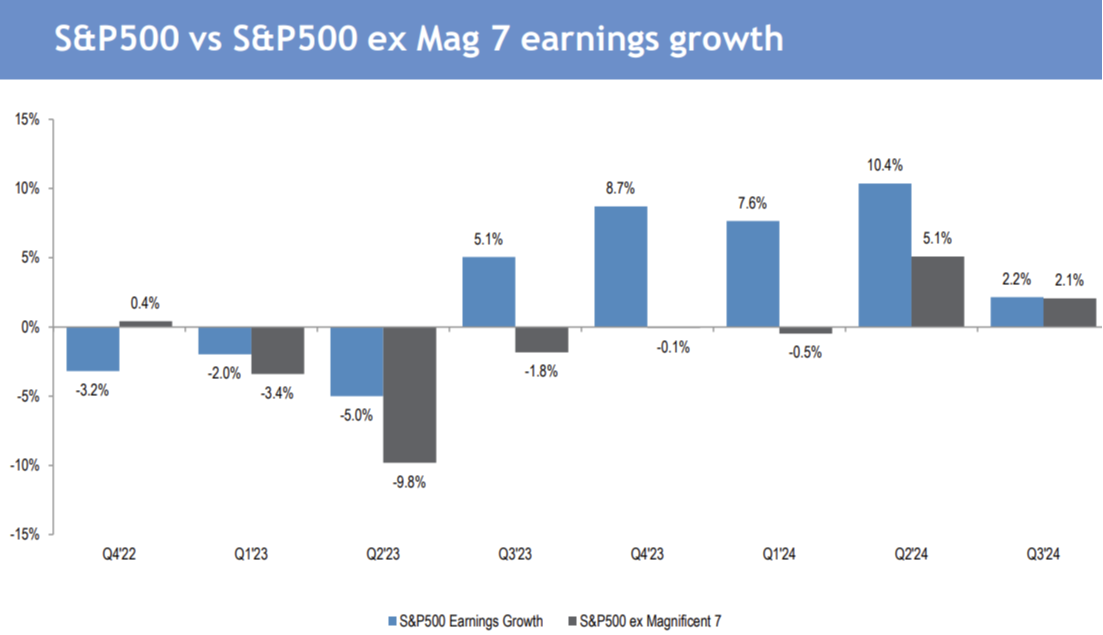

We are now fully in the throws of the third quarter earnings season. Of the 70% of S&P 500 companies that have reported earnings so far, 75% have reported a positive surprise on earnings per share, equal to the ten-year average, and 60% have reported a positive surprise on revenue. To date, the blended year over year earnings growth rate for the S&P 500 is 5.1% which, if it holds, would represent the 5th straight quarter of year over year earnings growth.5 For small caps, as of October 31st, 61% of Russell 2000 companies that already reported earnings surprised positively on EPS and 53% surprised positively on revenue. Communications Services lead the way within the index, outpacing all other sectors in surprise factor.6 As we have previously discussed, growth appears to be broadening out within large cap companies. Depicted in the graph below, non-Magnificent 7 companies have grown at the same rate as Magnificent 7 companies this earnings period.

Source: J.P. Morgan Markets7

Employment and Interest Rates

On November 1st, the U.S. Bureau of Labor Statistics released its October jobs report, announcing that 12,000 non-farm jobs were added, and that the unemployment rate remained 4.1%.8 Non-farm job additions were greatly affected by Hurricanes Helene and Milton as well as the Boeing machinists strike. Estimates place the strike’s effect on the jobs survey at approximately 38,000 jobs and expect that the impact of the hurricanes is somewhere in the ballpark of 50,000 jobs. An individual that was not working because of the strike or weather interruptions would have been counted against the non-farm payroll survey, but not the unemployment rate, explaining why that metric held steady at 4.1%.9 On Thursday, November 7, the Federal Reserve will announce another decision on rate cuts. It is expected that they will opt for a 25 basis-point reduction in interest rates. While the aforementioned job report made determining actual employment levels more difficult, it appears as though U.S job growth has gradually slowed. This is an expected result of Fed monetary policy. The Fed’s goal remains to counter this with rate cuts in the short and intermediate term.

Source: The Wall Street Journal.10 Not seasonally adjusted.

Source:

- Hatzius, J, et al. USA: Donald Trump Wins Presidential Election and Republicans Win Senate; House Still Unclear but Leans Republican. Goldman Sachs, November 6, 2024.

- IBID.

- Ip, G. What Trump’s Win Means for the Economy. The Wall Street Journal, November 6, 2024.

- Hussey, C, et al. Midday Market Intelligence: Post-Election. Goldman Sachs, November 6, 2024.

- Butters, J. Earnings Insight. Factset, November 1, 2024.

- Dhillon, T. Russell 2000 2024Q3 Earnings Dashboard. LSEG I/B/E/S, October 31, 2024.

- Matejka, M, et al. Equity Strategy: November Chartbook. P. Morgan Markets, November 4, 2024.

- U.S. Bureau of Labor Statistics. Employment Situation Summary. United States Department of Labor, November 1, 2024.

- Grossman, M. U.S. Job Growth Gradually Slowing Beyond Storm, Strike Disruptions. The Wall Street Journal, November 1, 2024.

- Lahart, J. At a Pivotal Moment, U.S. Economic Data Will Be a Mess. The Wall Street Journal, October 28, 2024.

Important Information

The Clifford Group LLC (“The Clifford Group”) is a registered investment advisor. Advisory services are only offered to clients or prospective clients where The Clifford Group and its representatives are properly licensed or exempt from licensure. The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. The Clifford Group and its advisors do not provide legal, accounting, or tax advice. You should consult your attorney or tax advisor. All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability, or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. The information contained above is for illustrative purposes only.

For additional information, please visit our website at www.thecliffordgrp.com.

Risk Disclosure

No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. All investments include a risk of loss that clients should be prepared to bear. The principal risks of The Clifford Group strategies are disclosed in the publicly available Form ADV Part 2A. Generally, among asset classes, stocks are more volatile than bonds or short-term instruments. Government bonds and corporate bonds have more moderate short-term price fluctuations than stocks, but provide lower potential long-term returns. U.S. Treasury Bills maintain a stable value if held to maturity, but returns are generally only slightly above the inflation rate. Investments in small-sized companies may involve greater risks than in those of larger, better-known companies.