October Market Insights

Positive Employment Numbers

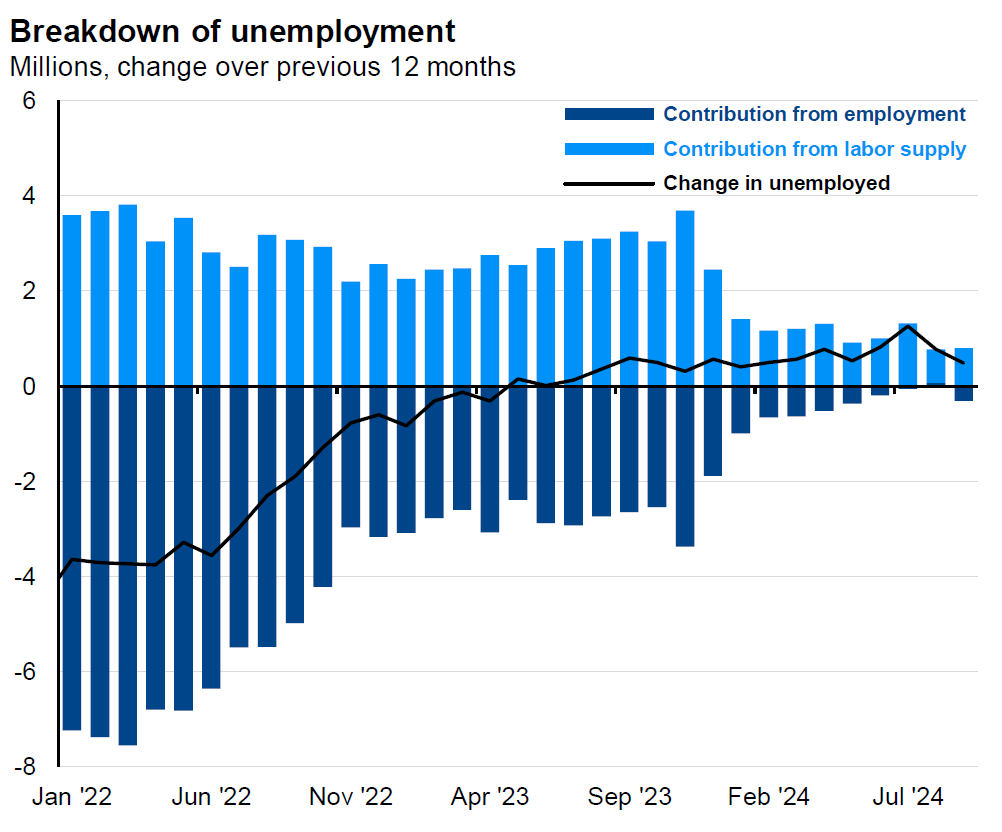

On October 4th, the U.S. Bureau of Labor Statistics announced September jobs numbers that were stronger than previous months suggested they might be. Total nonfarm employment added 254,000 jobs, and the unemployment rate ticked down to 4.1%.1 These numbers are strong in and of themselves and suggest that the Fed may be successfully satisfying its dual mandate after reducing interest rates and seemingly promoting employment. Furthermore, analysts see limited reason to expect further negative revisions of job statistics as GDP growth continues and healthy job openings remain.2 Finally, evidence also suggests that increases in unemployment over the last few months are largely driven by an increase in the labor supply, as opposed to a decrease in available jobs. Initial jobless claims and reported layoffs remain extremely low.3

Source: J.P. Morgan Asset Management.

Growth Outlook Steady

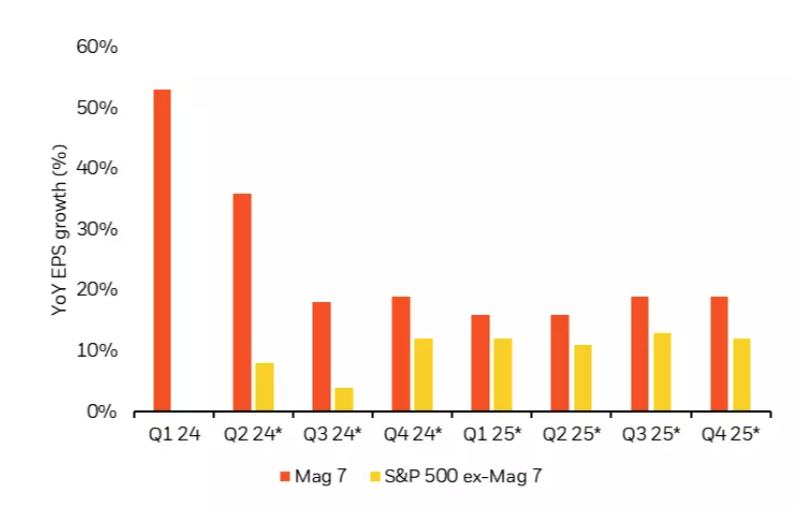

GDP growth expectations remain healthy looking into the next two years. Some estimates place 2025 real GDP growth at 2.3% and 2026 real GDP growth at 2.0%.4 Confidence in the market is now reflecting in EPS growth expectations as well. New forecasts place expected 2025 S&P 500 EPS growth at 11% year-over-year and 2026 growth at 6%.5 As shown in the chart below, EPS growth early in 2024 was consolidated largely to the Magnificent 7. Forward looking projections expect a meaningful broadening of this success, a positive sign for overall market health.6 In light of these positive forecasts, 12-month recession probability statistics decreased to the historical unconditional average.7

Source: BlackRock.

Opportunities

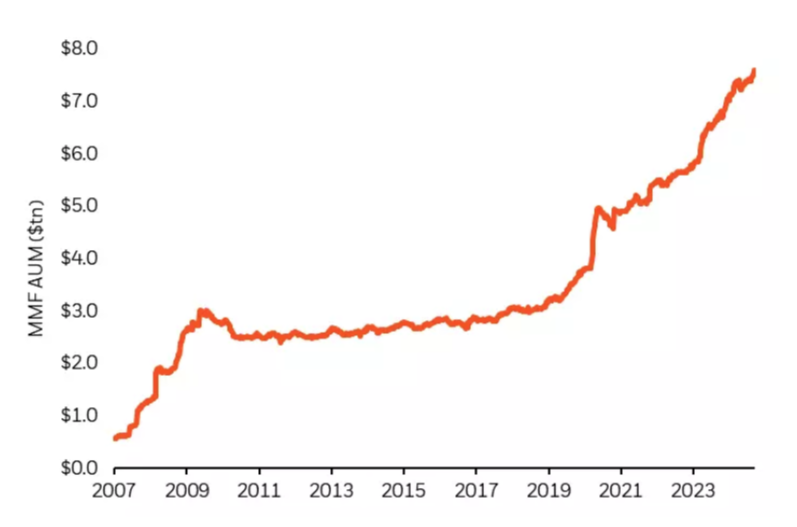

Within the context of sustained strong economic indicators, projected GDP and earnings growth, and short-term periods of volatility, there are opportunities to find value in the market. September and October historically tend to be volatile months.8 This volatility provides potential opportunity to put cash to work in response to slightly lower valuations. As seen in the chart below, money market fund account balances are sitting at record highs.9 Since the COVID-19 pandemic, investors have poured funds into these money market accounts. As rates begin to fall, however, it will be less attractive to leave money in money market funds. During cutting cycles, both fixed income and equity historically outperform cash.10 Capturing opportunity in both asset classes after periods of volatility could provide significant benefits in the long run.

Source: BlackRock.

Citations:

1) U.S. Bureau of Labor Statistics. Employment Situation Summary. Department of Labor, October 4, 2024.

2) Hatzius, Jan et al. Back on Track: Reassessing Labor Market Trends After the Employment Report. Goldman Sachs, October 6, 2024.

3) J.P. Morgan Asset Management. Weekly Market Recap. J.P. Morgan Asset Management, October 7, 2024.

4) Kostin, David et al. Raising our S&P 500 2025 EPS Growth Forecast to 11% and Lifting our 12-month Index Target to 6300. Goldman Sachs, October 4, 2024.

5) Ibid.

6) Chaudhuri, Gargi Pal and Akullian, Kristy. 2024 Fall Investment Directions. BlackRock, October 1, 2024.

7) Hatzius, Jan et al. Back on Track: Reassessing Labor Market Trends After the Employment Report. Goldman Sachs, October 6, 2024.

8) Chaudhuri, Gargi Pal and Akullian, Kristy. 2024 Fall Investment Directions. BlackRock, October 1, 2024.

9) Ibid.

10) BlackRock. Student of the Market, September 2024. BlackRock, September, 2024.

Important Information

The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your attorney or tax advisor. The views expressed in this commentary are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur. All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability, or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. The information contained above is for illustrative purposes only. The above targets are estimates based on certain assumptions and analysis made by the advisor. There is no guarantee that the estimates will be achieved.

The Clifford Group LLC (“The Clifford Group”) is a registered investment advisor. Advisory services are only offered to clients or prospective clients where The Clifford Group and its representatives are properly licensed or exempt from licensure. For additional information, please visit our website at www.thecliffordgrp.com.

Risk Disclosure

No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. All investments include a risk of loss that clients should be prepared to bear. The principal risks of The Clifford Group strategies are disclosed in the publicly available Form ADV Part 2A. Generally, among asset classes, stocks are more volatile than bonds or short-term instruments. Government bonds and corporate bonds have more moderate short-term price fluctuations than stocks, but provide lower potential long-term returns. U.S. Treasury Bills maintain a stable value if held to maturity, but returns are generally only slightly above the inflation rate. Diversification does not ensure a profit or guarantee against loss.

Risk associated with equity investing include stock values which may fluctuate in response to the activities of individual companies and general market and economic conditions. Although bonds generally present less short-term risk and volatility risk than stocks, bonds contain interest rate risks; the risk of issuer default; issuer credit risk; liquidity risk; and inflation risk.