September Market Insights

The U.S. Economy Remains Strong

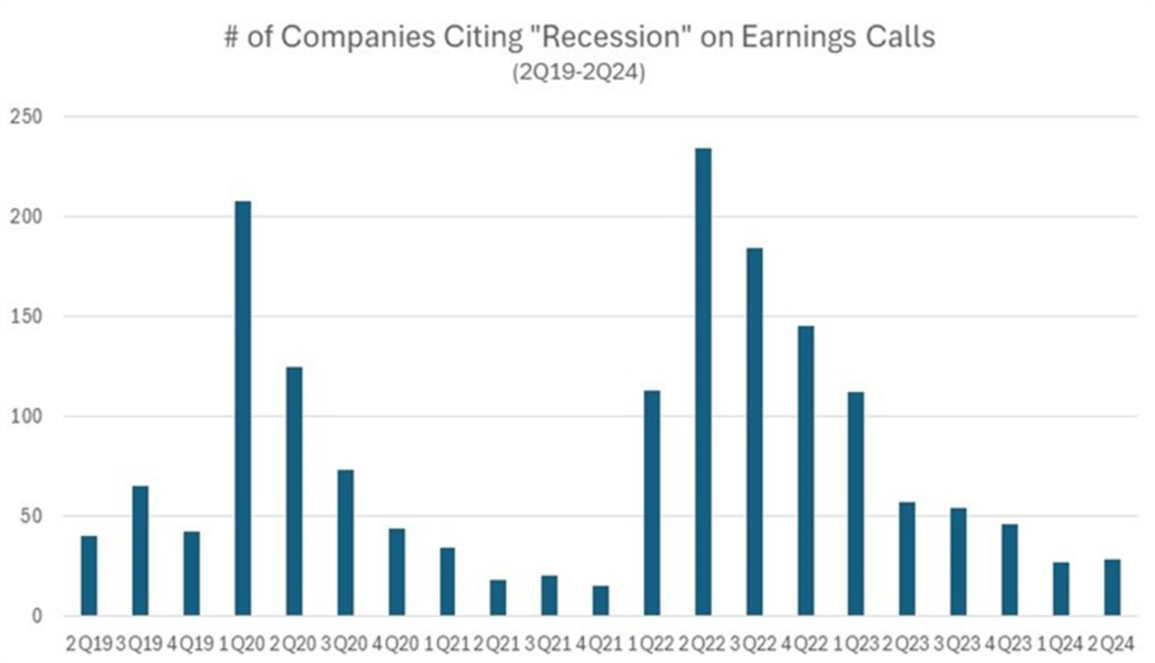

The last month has seen some limited market volatility, heavily anticipated employment numbers, and a very strong indication from the Chair of the Federal Reserve that interest rates will begin a cutting cycle starting in September.1 Amidst all the noise, we believe there is still considerable reason to be confident in the state of the economy. First, GDP projections remain positive. Real GDP grew at an annual rate of 3.0% in the second quarter of 2024.2 Projections for Q3 and Q4 currently sit between 1.5-1.9%.3 As interest rates decline, there is reason to believe that GDP growth beyond 2024 will remain positive as well. Second, jobless claims have increased but remain below last year’s levels,4 and though August’s employment numbers fell below expectations, they showed an increase in nonfarm jobs from July. Overall, unemployment decreased to 4.2%.5 Finally, major indices performed well on Q2 earnings. The S&P 500 reported earnings growth of 11.3%, the highest year over year growth since Q4 2021.6 The Russell 2000 Index closed out the earnings season with 66% of companies meeting or exceeding expectations on earnings per share and the index blended growth rate stood at 20.5%.7 A close look at the earnings calls of S&P 500 companies over the past two months shows that approximately the same number cited “recession” as did in Q1, lower than any other quarter since 2021.8 We value this as a sign that the overwhelming majority of major companies do not see indicators in their day-to-day business functions that would cause serious alarm.

Source: Factset.

Breadth of Opportunities

This past month demonstrated yet again that there are significant opportunities for diversified portfolios that include but are not limited to large cap growth stocks and the technology sector. Overall, the utilities sector reported the highest earnings growth of all 11 sectors in the S&P 500.9 In the Russell 2000 small cap index, the healthcare sector had the highest blended growth rate in revenue and second highest in earnings per share.10

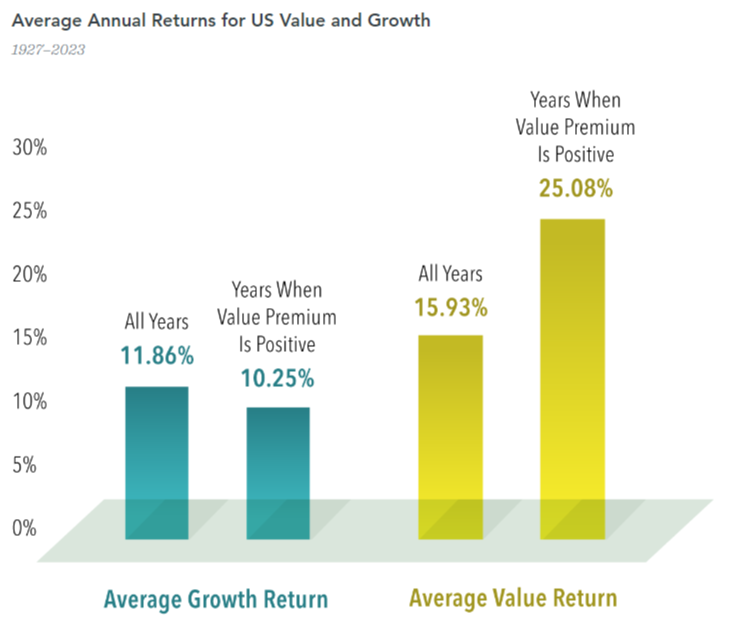

We see opportunity in value stocks as well. While growth stocks have dominated headlines this year, value stocks appear well positioned. When growth positions briefly faltered at the beginning of August, value stocks performed. More important to keep in mind, however, is that the market is not a zero-sum game between growth and value. As the chart below shows, the average annual return for value stocks is higher than that of growth positions. In years where value outperforms growth, growth still averages a positive return. There is, more often than not, upside to both styles.11

Source: Dimensional Funds.

We continue to see room for growth in small cap stocks. Small cap performance over the last two months has had its ups and downs. Small cap stocks performed very well in July (to the tune of 10.5%) before the employment numbers release in early August slowed them down.12 Conditions for small caps to succeed usually include a strong growth environment coupled with lower interest rates. Because we believe the economy is still strong, as rates come down small caps may have new opportunities for growth over time.

Volatility

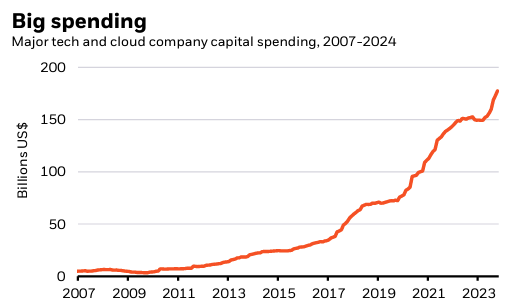

As we discussed in our August Market Insights, headline-grabbing earnings over the past few months have mostly focused on technology, artificial intelligence, and expectations surrounding when AI investment would start to show returns. We have seen in recent earnings calls, and outlined in the chart below, that capital spending on AI and AI supporting technology has continued.13

Source: BlackRock.

Because of the sky-high expectations associated with the enormous capital outlays and the breakneck pace of growth for AI stocks, we have seen sometimes counter-intuitive reactions to earnings announcements. When Nvidia released earnings and resoundingly beat expectations, the announcement was followed by sustained negative price movement. On the whole, we still see growth for tech and AI positions as part of a diversified portfolio but acknowledge that the actual returns on AI associated infrastructure development will take time to appear on paper.

As we inch closer to the Federal Open Market Committee’s decision on interest rates, which will be announced on September 18th, we may see continued volatility in the short term. The major question on many investors’ minds is how big of a cut will come this month. When we outlined this issue in our LinkedIn post this past week, we noted that the September 6 jobs report would help the FOMC decide the magnitude of the rate cut. With the jobs report showing improved conditions since July but falling short of expectations, we believe the most likely scenario is a standard 25 basis point cut this September to start a gradual rate reduction cycle. Shortly after the release of the jobs report, John Williams, the President of the Federal Reserve Bank of New York and a voting member of the FOMC, noted that the Fed could now focus on lowering rates “over time”.14

Sources:

1) Chair Powell, Jerome. Review and Outlook. Board of Governors of the Federal Reserve System, August 23, 2024.

2) Bureau of Economic Analysis. Gross Domestic Product (Second Estimate), Corporate Profits (Preliminary Estimate), Second Quarter 2024. S Department of Commerce, August 29, 2024.

3) Federal Reserve Bank of Philadelphia. Third Quarter 2024 Survey of Professional Forecasters. Federal Reserve Bank of Philadelphia, August 9, 2024.

4) Advisor Outlook September 2024. BlackRock, September 4, 2024.

5) U.S. Bureau of Labor Statistics. Employment Situation Summary. U.S. Department of Labor, September 6, 2024.

6) Butters, John. Earnings Insight Infographic: Q2 2024 By the Numbers, Factset, September 5, 2024.

7) Dhillon, Tajinder. Russell 2000 2024Q2 Earnings Dashboard. LSEG I/B/E/S, September 5, 2024.

8) Butters, John. Earnings Insight. Factset, August 16, 2024.

9) Butters, John. Earnings Insight Infographic: Q2 2024 By the Numbers, Factset, September 5, 2024.

10) Dhillon, Tajinder. Russell 2000 2024Q2 Earnings Dashboard. LSEG I/B/E/S, September 5, 2024.

11) Crill, Wes. Value Can Pop Without a Growth Drop. Dimensional, August 29, 2024.

12) Chaudhury, Gargi Pal. Navigating Market Volatility: Insights for Investors. iShares, August 14, 2024.

13) Bovin, Jean; Harasim, Beata; Arevalo, Carolina Martinez. Weekly Commentary. BlackRock, September 3, 2024.

14) Uberti, David. Employers Added 142,000 Jobs, Missing Expectations, Though Unemployment Ticked Down. The Wall Street Journal, September 6, 2024.

Important Information

The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your attorney or tax advisor. The views expressed in this commentary are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur. All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability, or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

Risk Disclosure

Generally, among asset classes, stocks are more volatile than bonds or short-term instruments. Government bonds and corporate bonds have more moderate short-term price fluctuations than stocks, but provide lower potential long-term returns. U.S. Treasury Bills maintain a stable value if held to maturity, but returns are generally only slightly above the inflation rate. Risk associated with equity investing include stock values which may fluctuate in response to the activities of individual companies and general market and economic conditions. Diversification does not ensure a profit or guarantee against loss. Risk associated with equity investing include stock values which may fluctuate in response to the activities of individual companies and general market and economic conditions. Investments in small-sized companies may involve greater risks than in those of larger, better known companies.